I have a confession. I own shares in Apple Inc. (NASDAQ:AAPL). There, I said it.

Not only that, I added modestly to my position this morning, May 2, at a price just slightly below $93. In admitting this, why do I feel like I’m guilty of something – at the very least naiveté, and perhaps even rank stupidity?

Well, because a lot I read these days tells me that I am. I mean, right here on Seeking Alpha, this article tells me that I am placing “blind faith” in the company and possibly even engaged in “magical thinking.” Another tells me that, as an Apple shareholder, I’m a victim of a capital return program that is a “complete joke.” And finally, this article informs me that Apple is losing, or will lose, ground to Samsung.

Listen, I will be the first to admit that, at least from the standpoint of attention-grabbing headlines, last week wasn’t a great week for Apple. The earnings release was generally considered disappointing, as the company reported its first year-over-year (YOY) revenue decrease in 13 years. A mere two days later, the news that Carl Icahn no longer holds a position in the company provided more drama.

Why, oh pray why, then, would I not only continue to hold Apple at this point, but even add to my holdings? Simply put, because beauty is in the eye of the beholder.

What is it that I think I am seeing? Where is Apple’s beauty, to me?

First of all, let me state right up front that I don’t view Apple as a growth stock. I believe those days are likely in Apple’s past. I’m not sure they will ever come up with as groundbreaking an innovation as the iPhone has proved to be. No, at this point, I’m looking at Apple as a long-term value holding.

Let me attempt to explain why. I will start by featuring a perspective that I feel may have been missed in other articles as well as a few thoughts on Apple’s cash hoard, dividend and the future potential for realization of such value.

Stepping Back For A Longer View

As featured above, perhaps the most dramatic news from the earnings release was that YOY revenue decrease. I listened to the call, however, and picked up on the following statements.

First, from Tim Cook:

. . . From an upgrade perspective, during the first half of this year the upgrade rate for the iPhone 6s cycle has been slightly higher than what we experienced in the iPhone 5s cycle two years ago, but it is lower than the accelerated upgrade rate that we saw with iPhone 6, which as you know was a big contributor to our phenomenal revenue growth a year ago.

Next, from Luca Maestri:

For details by product, I’ll start with iPhone. We sold 51.2 million iPhones in the quarter compared to 61.2 million in the year-ago quarter, a decline of 16%. It was a particularly challenging comparison to the record quarter a year ago, when iPhone sales grew 40% . . .

Let’s quickly summarize, from Maestri’s statement. iPhone sales experienced “a decline of 16%” when compared to last year “when iPhone sales grew 40%.” Or, as Cook referred to it, a comparison against the “accelerated upgrade rate that we saw with the iPhone 6… a big contributor to our phenomenal revenue growth a year ago.”

Anyone who has even casually followed Apple for the last couple of years knows what a big deal the iPhone 6 was. After years of resolutely sticking with a smaller screen size, Apple finally yielded to market demand and released the iPhone 6, with its 4.7-inch screen, and its bigger brother, the iPhone 6 Plus, sporting a 5.5-inch screen. This phone immediately generated, to use Cook’s word, “phenomenal” demand. Scores of customers snapped up both variants of the iPhone 6, to the point that Apple experienced great difficulty in keeping up with the demand. The iPhone 6s, as a mid-cycle upgrade, has not matched that level of demand.

But wait a minute. What if we set aside the “phenomenal” circumstances around the iPhone 6 release and take a little longer view backwards in time? What if we compare the 2016 report against 2014 and 2013? If nothing else, that at least gives us one more perspective by which to evaluate Apple.

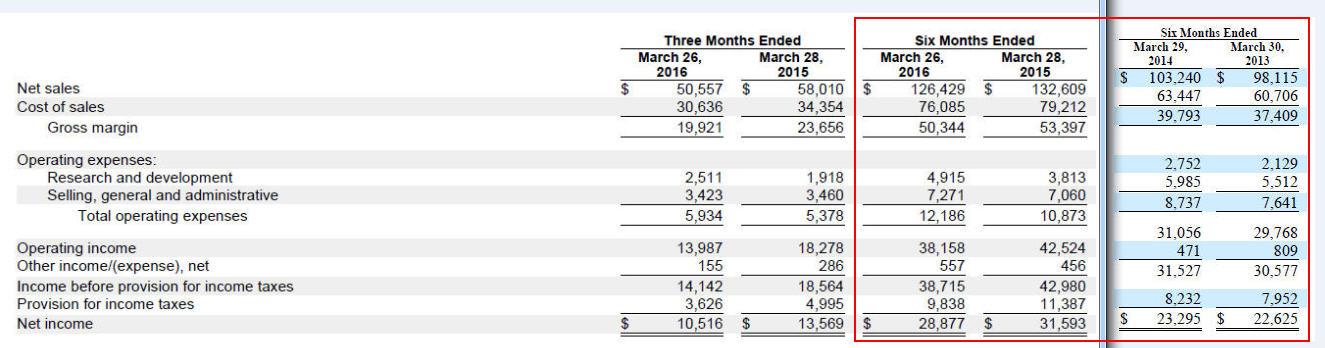

So, here it is. I cobbled together a couple of screen shots of the Apple 10-Qs for Q2 2016 vs. Q2 2014 (hence the different fonts). Have a look at the “three months ended” comparisons for 2016, 2015, 2014, and 2013.

Click to enlarge

Click to enlarge

Next, here is the same comparison, only using figures for the “six months ended:”

Click to enlarge

Click to enlarge

As can be seen, if you set aside 2015 for just a minute, a picture emerges of what I would describe as slow, steady progress.

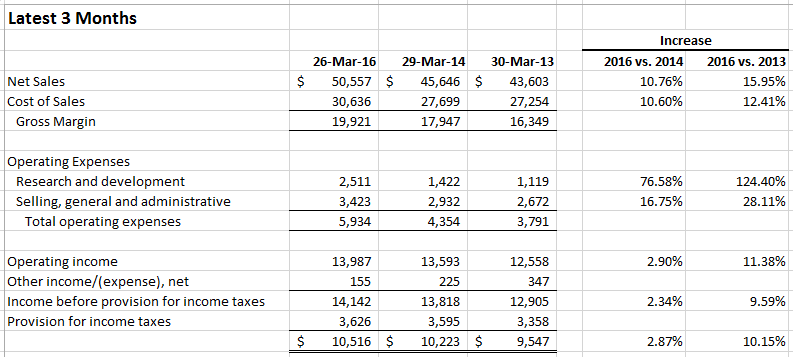

Now that I have documented the data for you, have a look at two little schedules I generated in Excel. In these, I left out the 2015 column and just did a little comparison of 2016 against 2014 and 2013. I also included formulas on selected lines to get a peek at the respective growth rates.

First, the “three months ended” summary.

Click to enlarge

Click to enlarge

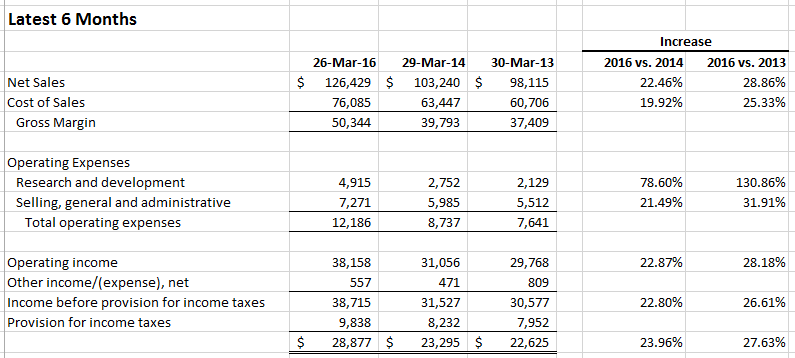

Now, the “six months ended” summary.

Click to enlarge

Click to enlarge

Given this perspective, a few observations:

- Looking at the “latest six months” variant, we see net sales growth of 22.46% since 2014 and 28.86% since 2013. Even looking at the more disappointing “latest three months” variant, these values stand at 10.76% and 15.95%, respectively. Before you dismiss Apple completely, ask yourself how this level of growth might compare against other leading companies over this time period, especially when factoring in both a difficult economic environment as well as the impact of the strong dollar on currency translation of overseas sales.

- The “operating income” line does not fare quite as well, although it still registers growth. However, when you look a little closer, you will notice that a large reason for this is that Apple’s spending on research and development is actually up quite significantly over that span, over 100% since 2013 in both variants. That tells you that Apple is still spending money on innovation.

My point? Simply to take a second look at a longer time frame and ask yourself if you feel that Apple’s growth is at least reasonable for a company with the P/E that Apple is carrying at current prices.

The Dividend Increase

Now let’s move on to uses of cash. In recent years, Apple has both engaged in share buybacks and increased its dividend.

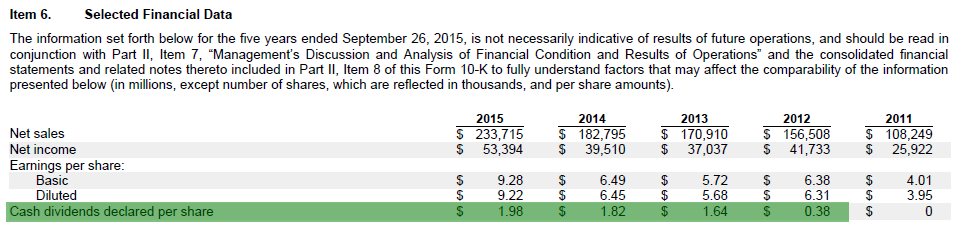

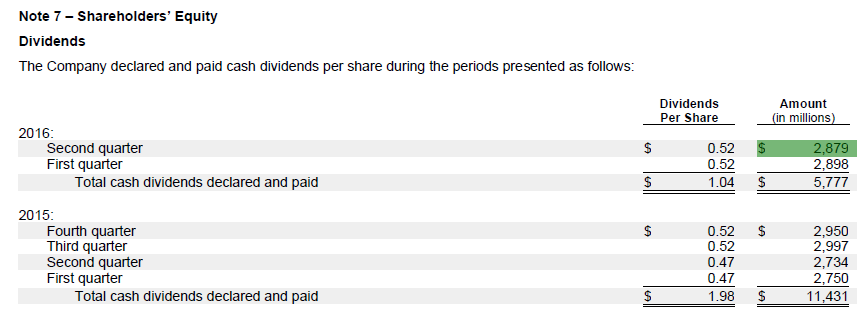

For purposes of this article, I would like to focus on recent dividend history for just a minute. Here, from the 2015 10-K, is the most recent chart.

Click to enlarge

Click to enlarge

You don’t need me to do an Excel sheet for this one. Just eyeballing the numbers, you can see that Apple has increased their dividend between 8-10% each year since they initiated it back in 2012.

This year is no exception. Apple raised their quarterly dividend from .52 to .57, virtually a 10% increase. Further, they have publicly stated their intent to raise it each year moving forward.

What basis, though, can you have for confidence that they will? Well, one method commonly used is to take a look at the dividend coverage ratio. Essentially, this takes a look at a company’s profits, minus any dividends payable on preferred shares, to evaluate how many times over it could pay its dividend. So, for example, if a company had profits of $100, and had to pay dividends of $80, investors might be uncomfortable. After all, how much would profits have to drop before that dividend could not be paid?

Here, again, from the 10-K, is data for Apple. For now, just focus on the number I highlighted in green – what Apple paid in Q2 2016:

Click to enlarge

Click to enlarge

If you look back at the report even for Apple’s “disappointing” recent quarter, you will notice that profit after tax was $10,516 million. In other words, even with the 10% dividend increase, Apple will have to pay out somewhere between $3,100 and $3,200 million per quarter, or about 30% of their Q3 profits.

In addition to all of this, Apple’s cash hoard makes the future payment of such dividends, in my view, about as secure as anything you may find, including certain government agencies.

Speaking of Apple’s cash hoard, let’s talk about that next.

Apple’s Cash Hoard, Repatriation, and Corporate Tax Reform

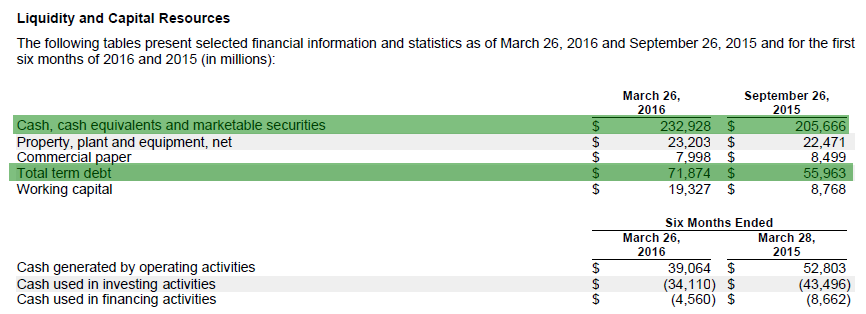

Here is a picture of the “Liquidity and Capital Resources” section of Apple’s Q2 2016 10-Q.

Click to enlarge

Click to enlarge

Essentially, as of March 26, 2016, we have $232.9 billion of cash, cash equivalents and marketable securities, offset by $71.9 billion in total term debt, or a net of $161.0 billion.

However, as shown in a later paragraph in the same section, $208.9 billion is held offshore, and subject to U.S. income taxation.

Click to enlarge

Click to enlarge

At the current time, were Apple to repatriate those funds, it is true that these would be taxed at a 35% rate. In other words, of that $208.9 billion, a little less than $136 billion would be realized by the company and, therefore, its shareholders.

However, if you have been keeping current with business news, likely you are aware that U.S. corporate tax reform is a lively issue these days. As just one example of media coverage, take a look at this February 2015 article from The New York Times. After featuring some of the problems inherent in the current system, and some ideas for reforming them, the article offers this comment:

What the reforms would do is foster a change in corporate thinking. Companies would make their financing and investing decisions with more of an eye to pretax profits rather than tax planning. American companies tie themselves in knots to avoid bringing foreign profits home. They borrow money instead of repatriating foreign profits to finance domestic investment, or they invest offshore profits in foreign businesses simply to avoid triggering American taxes. All that tax planning costs money and sways companies from investing in the opportunities that generate the highest pretax profits.

Apple, along with several other companies, have recently lobbied either for such reform, or at the very least some window to bring overseas cash back into the U.S. at a greatly reduced tax rate. Clearly, no one would be as big a beneficiary of this as Apple.

As a number to ponder, what if even a temporary window opened to repatriate cash to the U.S. at a 15% tax rate, the rate that most taxpayers currently pay on both preferred dividends and long-term capital gains? With a $208.9 billion foreign cash hoard, such a difference would be worth almost $42 billion to Apple shareholders.

Summary and Conclusion

What is your view of Apple? Certainly, you can read much at the present time that maligns the company. You can read about how it has lost its innovative edge. You can read about market saturation, how Apple’s products are not as good as competitive products, how they are too expensive, and all manner of related criticism. And I don’t intend to waste one minute here arguing with any of it. You are free to read these views and draw your own conclusions.

And yes, as I made clear in my introduction, I think it is absolutely clear that Apple is not the growth company it once was. Last year’s tremendous iPhone 6 results aside, it may be the case that these cannot be repeated.

But perhaps beauty is in the eye of the beholder. In this article, I have attempted to show that, when viewed through the perspective of a longer lens, Apple is still growing, albeit at a modest pace. For me, I look at it as more of a value play, with great products, a growing revenue stream from those products in terms of apps, music, and other services, what appears to be solid financial management, and even the possibility of positive surprise – for example if U.S. corporate tax reform opened a window for Apple to repatriate some of that offshore cash at much better terms.

I’m interested to see the comments I receive.

In any event, I will hopefully get back to my main focus – writing about ETFs and diversified, low-cost portfolios. In the meantime, as always, I wish you . . .

Happy investing!

Authors Note: If you like my work, I would be deeply indebted, and highly grateful, if you could be sure to follow me here on Seeking Alpha, as well as feature my work to friends, colleagues and/or relatives who may be interested in the subject matter. Other than the time you invest to read, there is no other cost for the work that I do. Your support will enable me to continue my efforts.