It’s fashionable for manufacturing CEOs to talk about “reshoring,” but is it actually happening?

Photographer: Luke Sharrett/Bloomberg

Photographer: Luke Sharrett/Bloomberg

To get Brooke Sutherland’s newsletter delivered directly to your inbox, sign up here.

Speculation has swirled this past year that supply-chain disruptions from the U.S.-China trade war and Covid-19 pandemic would inspire companies to bring manufacturing work back to North America. Is it actually happening, though? There’s some evidence that it is: Taiwan Semiconductor Manufacturing Co. in May unveiled plans for a $12 billion chip factory in Arizona and Samsung Electronics Co. is reportedly contemplating spending more than $10 billion to build a rival cutting-edge plant in Austin, Texas. Becton Dickinson & Co. is investing in additional factory capacity for syringes in Nebraska (with some help from the government). Tool-maker Stanley Black & Decker Inc. has had a “Built-in-the-USA” initiative for years that appears only to have accelerated in the wake of Trump’s myriad trade battles.

But that’s more or less where the examples end. The industrial companies spending the most time talking about “reshoring” these days seem to be the factory-automation equipment makers, and they have a vested interest in making this trend a reality. That’s because most manufacturers would need to invest in robots and software to make a move to the U.S. cost-effective. And it may just be too early: Many industrial companies plan to increase their capital spending this year back to pre-pandemic levels and perhaps some of that money will find its way to new manufacturing lines. But at this point, it’s hard to tell if we’re looking at a paradigm shift or just some tinkering around the edges in select industries.

Because life sciences is often highlighted as a sector where reshoring is gaining momentum, I thought it might be helpful to actually ask a CEO of a life-sciences company what he thinks. “To reshore is much more difficult than people give it credit,” Dr. Udit Batra, chief executive officer of lab-equipment manufacturer Waters Corp., said in an interview. A decentralized supply-chain that takes advantage of specific skillsets in different jurisdictions works better for a company like Waters that manufactures high-tech products, he said. For example, the company’s mass spectrometry systems are produced out of the U.K. and Ireland, but it outsources some parts manufacturing work along the way to trusted contractors before putting the products back in the hands of its own engineers, who perform final assembly, calibrations to customer specifications and quality-control procedures. It relies on contract manufacturers in Singapore for certain work on its liquid chromatography instruments.

“Our supply chains are so connected globally and we realize such efficiencies,” Batra said. The company localizes its processes in more narrow ways — data-privacy laws are different between the U.S., U.K. and China, for example, so Waters might need three e-commerce teams. But “I don’t see a practical answer to making complex products in one spot,” Batra said. “It’s not a logical discussion. Economically, it doesn’t make sense.”

This is just one example, but it provides interesting perspective. Part of the gap between the enthusiasm around reshoring and the relative dearth of high-profile examples may also be a misunderstanding of who is going to be doing the relocating. Perhaps the issue isn’t that large manufacturers aren’t localized enough, but that smaller suppliers aren’t globalized enough, Barclays Plc analyst Julian Mitchell said in a December interview.

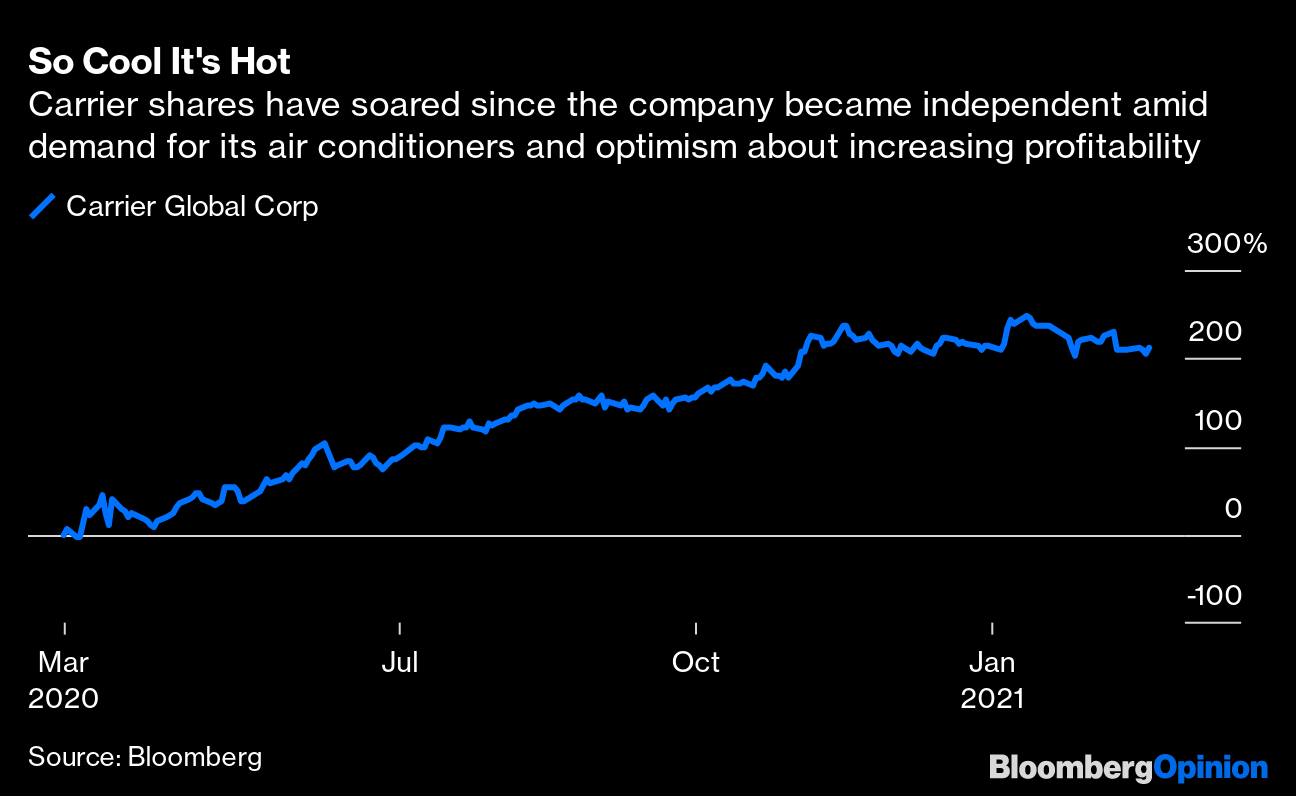

Air conditioner-maker Carrier Global Corp., for example, is undertaking a major reform of its supply chain as part of a $700 million cost-savings program. Part of the process is about getting better pricing and more alignment on quality control and inventory management, but the company is also keen to winnow down the number of vendors it relies on. Carrier directly purchases components from about 4,000 suppliers with frequency, an inefficient legacy of myriad acquisitions over the years, Carrier CEO Dave Gitlin said in an interview. It feels weird in this time of pandemic disruption to be talking about fewer suppliers, but Carrier doesn’t necessarily need to work with multiple companies to build supply-chain resiliency for a specific part, Gitlin said. It just needs whatever company it does work with to have multiple ways of delivering the order. Carrier has for years operated on the philosophy of producing products in the regions where it sells them, with facilities in North Carolina, Georgia and Mexico. It might shift to one supplier from three for a certain input, if that vendor can put its production sites nearer to its own, Gitlin said.

So Cool It’s Hot

Carrier shares have soared since the company became independent amid demand for its air conditioners and optimism about increasing profitability

Source: Bloomberg

Rival climate-control company Trane Technologies Plc is in the process of its own supply-chain overhaul as part of a $160 million cost-savings program. Some of this is about consolidating and modernizing IT systems; the company could cut as much as 50% of the applications it uses, CEO Mike Lamach said in an interview. But Trane also wants to re-evaluate how it makes sourcing decisions in the first place and curb the proliferation of options. “We’re not just going from one supplier to another or asking to reduce costs; we’re redesigning some of the systems to get more uniformity in the product,” Lamach said. “We might use a hundred different motors and fan systems, but the reality is we probably need 20. It takes a lot of engineering and testing to change those other 80, but if you put people on the same page and get them all lined up, you can go through it quickly.” The company still plans to rely on multiple vendors for the more commoditized parts it doesn’t make in house, but it’s “always biased for a closer supplier than one that’s geographically further away,” Lamach said. There are fewer headaches from currency swings and also sustainability benefits because not as much fuel is needed to get parts from point A to point B, he said.

Deals, Activists and Corporate Governance

Regal Beloit Corp. is combining with Rexnord Corp.’s process and motion-control segment — which includes products such as bearings, gears and conveyor belts — in a tax-friendly reverse Morris trust transaction. The deal values the Rexnord business at $3.69 billion. The Rexnord assets are highly complementary to Regal Beloit’s power transmission business but add more exposure outside of North America and in faster-growing markets like renewable energy, automation and e-commerce. Regal Beloit is targeting $120 million in annualized cost savings from the deal. Rexnord will be left with a water-management business that sells everything from drainage systems and valves to toilets, sinks and hand dryers. It’s a less economically volatile business than bearings and gears, and one that’s benefiting from pandemic trends around touchless bathroom fixtures.

One interesting twist in this combination: Regal investors are expected to own 61.4% of the combined entity, while Rexnord holders will own 38.6%. For the reverse Morris trust deal structure to work, typically shareholders of the target entity (in this case, Rexnord) need to own more than 50% of the combined company. But Regal has found a loophole, thanks to the large degree of overlap between its shareholder register and that of Rexnord. Because some of its investors are also Rexnord investors, they essentially gain ownership in the new entity in two ways and their Regal stakes apparently can count toward the 50%-plus threshold for tax purposes. Whatever remaining gap there is after overlapping shareholders are accounted for at the time of closing will be addressed through a special dividend of as much as $500 million for Regal shareholders and a corresponding bump-up in equity ownership for Rexnord investors.

Boeing Co. is making more board changes. Two of the company’s longest-serving directors, former Medtronic CEO Arthur Collins Jr. and former U.S. Trade Representative Susan Schwab, will retire when their current terms expire in April. Boeing didn’t announce any immediate replacements but said it continues to identify “a pipeline of diverse candidates with appropriate expertise who bring qualified perspectives.” A smaller, more focused board with the necessary skillsets to steer Boeing through the dual crises of the pandemic and 737 Max debacle wouldn’t be a bad thing; General Electric Co. significantly cut its director count as CEO Larry Culp undertook a turnaround push. Boeing in January announced that Lynne Doughtie, the first woman to be elected U.S. chairman and chief executive officer of KPMG, would replace Caroline Kennedy on the board. In total, eight directors have stepped down since regulators grounded Boeing’s Max in March 2019.

Raytheon Technologies Corp. has reportedly raised objections with antitrust officials over the planned takeover of Aerojet Rocketdyne Holdings Inc., a key supplier for propulsion systems. Raytheon told the U.S. Federal Trade Commission that Lockheed Martin Corp.’s $4.4 billion deal to acquire Aerojet Rocketdyne risks exposing its intellectual property to a rival and would create a duopoly of missile-makers with in-house engine units, a person familiar with the matter told Bloomberg News. Speaking at a Barclays conference this week, Lockheed chief financial officer Ken Possenriede said the transaction should benefit all of Aerojet’s customers with a lower-cost, higher-quality product. The regulatory approval process for this deal will be an interesting test of the FTC’s stance on vertical integration under the Biden Administration. Acting chair Rebecca Kelly Slaughter has advocated for vertical deals getting a closer look. Bloomberg Intelligence analyst Douglas Rothacker said Raytheon’s objections aren’t “necessarily a deal killer,” but regulators may ask for some concessions.

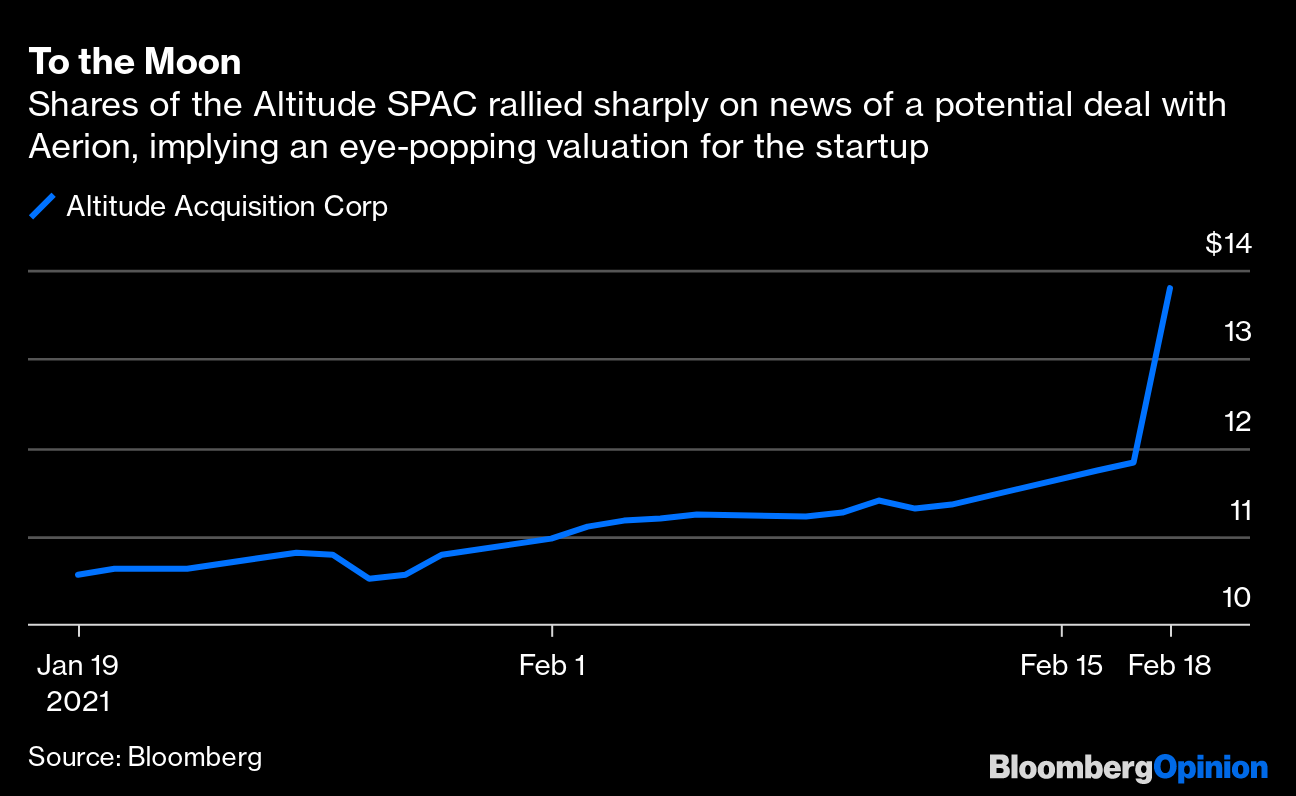

More SPACs. Aerion Corp., which designs supersonic planes and counts Boeing as an investor, is in talks to go public through a merger with special purpose acquisition company Altitude Acquisition Corp., people with knowledge of the matter tell Bloomberg News. The transaction would value the combined entity at about $3 billion. The company is aiming to start production on a supersonic business jet powered by GE jet engines in 2023. If that doesn’t pique your interest, there’s also going to be an electric jet-ski SPAC. Taiga Motors, which also makes electric snowmobiles, will merge with a blank-check firm sponsored by Canaccord Genuity Group Inc. for an implied market value of C$537 million ($422 million). And in case you missed it, my colleague Chris Bryant’s take on the risks of investing in the plethora of futuristic air-travel technology companies that have gone public recently is worth a read.

To the Moon

Shares of the Altitude SPAC rallied sharply on news of a potential deal with Aerion, implying an eye-popping valuation for the startup

Source: Bloomberg

Ingersoll Rand Inc. is selling a majority stake in its high-pressure pumps business to private equity firm American Industrial Partners for $300 million in proceeds. With the divestiture, Ingersoll will get less than 2% of its revenue from the exploration and drilling part of the oil and gas market. This volatile business has been unhelpful for Ingersoll’s valuation and its appeal to environmentally focused investors. Ingersoll will retain a 45% equity stake in the business.

Bonus Reading

Texas, California Blackouts: A Song of Ice, Fire: Liam Denning

Pfizer, BioNTech Ask FDA to Approve Easier Vaccine Storage

Relentless Home-Renovation Boom Sends Lumber Price to Record

Amazon and UPS Are Kingmakers in EV Bubble

BlackRock Wagers on ESG. Now It Needs a Payoff: Nir Kaissar

Porsche Listing Talks Signal Auto Upheaval Is Just Starting

3M Plans $1 Billion in Spending to Cut Emissions, Save Water

The Auto Industry Bets Its Future on Batteries

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Brooke Sutherland at bsutherland7@bloomberg.net

To contact the editor responsible for this story:

Beth Williams at bewilliams@bloomberg.net