Bonal Industries (OTCPK:BONL) has been written up previously on S.A. and we suggest reading those articles in addition to this one, particularly with respect to company history/management/shareholder friendliness. We have had this name on our watch list for some time, but it has been too expensive in our view. Following tough earnings last quarter with revenues down by more than 50% and no profitability the stock has begun to crater, trading as low as $1.05/sh (very temporarily), and is currently sitting at $1.70/sh, we think the name is interesting at these levels. That said, this is an extremely illiquid stock and it can be challenging to build a position, also the bid-ask spread is very wide, so be sure to use limit orders if purchasing. While we typically write about common dividend stocks occasionally a high yielding micro-cap such as BONL pops up, and often these end up being the more rewarding ideas. Follow us here on Seeking Alpha for more dividend ideas.

Source: meta-lax.com

Bonal is the patent holder and world’s leading provider of sub-harmonic vibratory stress relief and weld conditioning technology. They sell their products globally serving the aerospace, armament, automotive, petroleum, die-casting, mining, racing, machine tool building, plastic molding, shipbuilding, and welding industries. The core product, Meta-Lax, is used to eliminate thermal stress in metal parts, thereby preventing warping and cracking, at a fraction of the energy and monetary costs of competing technologies. The company is producing a new computerized unit, the Meta-Lax Model 2800, which they hope will become the industry standard and expect it will continue to support the business in coming years. It’s a niche business, but it’s the king of it its niche and that’s an important place to be.

In our eyes, the Model 2800 can’t come soon enough; it’s amazing the previous model, the 2400 still saw the demand it did, from a utilitarian perspective it worked well enough, but it is certainly in need of some updating. You can get an idea of the interface in this comical tutorial video, hopefully the new unit will be run using a modern interface and perhaps discussing the product rather than music. While they are at it the website could use a touch up as well to get rid of the 90’s feel.

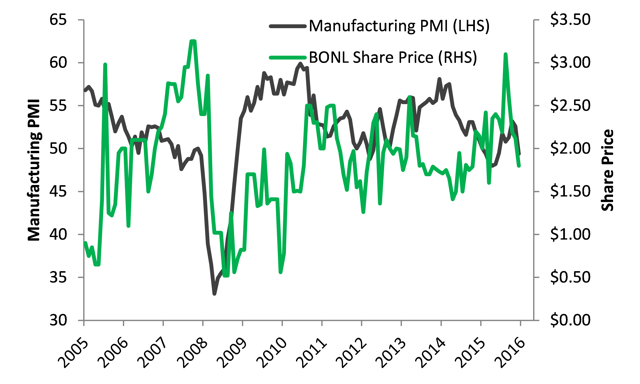

About half of Bonal’s annual business is repeating (42% in both fiscal 2015 and 2016). And about 80% of its revenues are in the U.S. mostly stemming from equipment sales. As such, the business will remain levered to the health of the U.S. metalworking market and by extension the health of the U.S. manufacturing sector. The chart below shows Bonal’s share price performance overlaid with the U.S. Manufacturing PMI which is an indicator of purchases in the manufacturing space. While the two are not particularly correlated, one reason for this is the illiquidity of Bonal shares.

Data source: Bloomberg

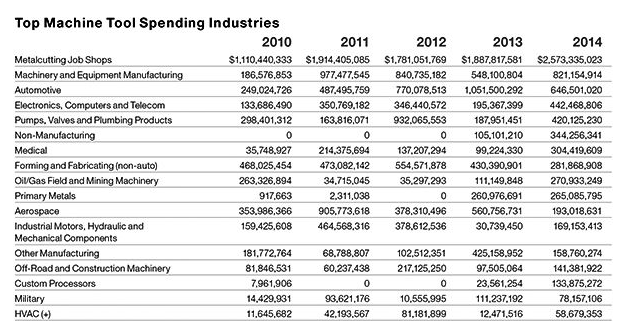

One of the industries that Bonal sells to is machine tool building, and looking deeper into this segment gives an indicator of where capital is being spent in Bonal’s other segments. Many of the same companies that need machine tools are producing high end equipment that also needs to avoid thermal stress. So it follows that higher machine tool spending should also be good for Bonal.

We recommend reading the End Market Spending Trends from the link above. It points to the rise of demand from Job Shops as much of the metalworking work is being shifted from industries such as Aerospace into these job shops. It also points to Electronics being positively impacted by reshoring and high growth in storage and transportation for natural gas. While oil/gas spending will be much lower since 2014, we think some of the other positive trends remain.

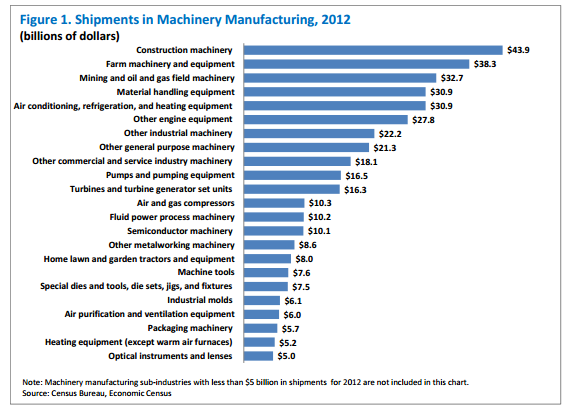

The problem with Bonal, evidenced by Q1-17 results, is that the North American metalworking industry as a whole is not doing well. The chart below shows the major machinery categories, many of the top buckets are performing terribly in today’s market. Low crop prices mean farmers spending on capital items such as tractors and farm machinery is deferred, they simply do not have the excess income to make these purchases, this is why we see companies such as Deere not performing particularly well. Mining and oil and gas machinery is performing poorly in today’s market as well, while we have seen a small comeback in both over the past year, the sectors remain depressed, and oil and gas capex has been cut sharply following the collapse of the global energy complex. While the likelihood of these industries to recover eventually is high, the likelihood of it being a near-term recovery is low. In other words, this year is likely to remain tough for Bonal.

Source: Industry primer

The company prides itself on a dozen profitable years across varying market conditions, and has paid dividends for 11 consecutive years. Despite a solid history of paying dividends, the number of annual payments has been lumpy, and one cannot necessarily extrapolate the LTM dividend payments to determine a forward yield. While some dividend is likely this year, with one bad quarter already behind them, it is unlikely we see more than one or two $0.05/sh payments this year, indicating a forward yield is likely in the 3% to 6% range, still fair. If the metalworking market turns around we could easily see $0.20/year dividends return which would be a catalyst for the stock.

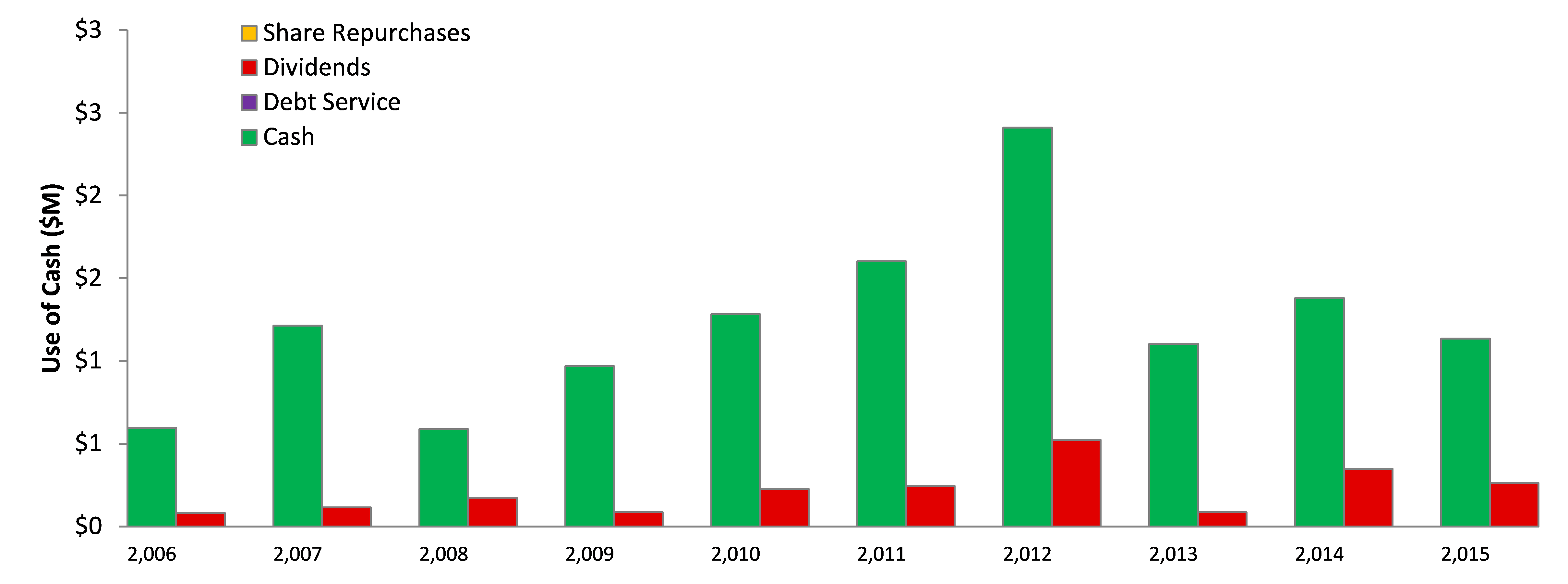

Use of Cash: the use of cash test provides a visual overview of the various cash uses that a company has been allocating cash towards. It shows the relative size of the cash uses versus the outstanding cash balance available to the company. It is a quick and simple way to view how the company has used its cash over the past 10 years, and is indicative of what the company may do in the next 10 years with its cash reserves. We examine dividend payments to all shareholders (including payments to preferred dividend holders) as well as net repurchases which includes equity issued via stock option plans etc… as well as interest payments on debt, this offers a more wholesome view of how the company allocates capital.

Click to enlarge

Click to enlarge

From a use of cash perspective, Bonal’s chart is very simple. They are conservative, have never used leverage, and have been consistent dividend payers but have paid inconsistent levels of dividends. Similar to the past, we anticipate no leverage and no share repurchases going forward, dividends are likely to continue, although they are likely to be smaller this year than in the last couple years.

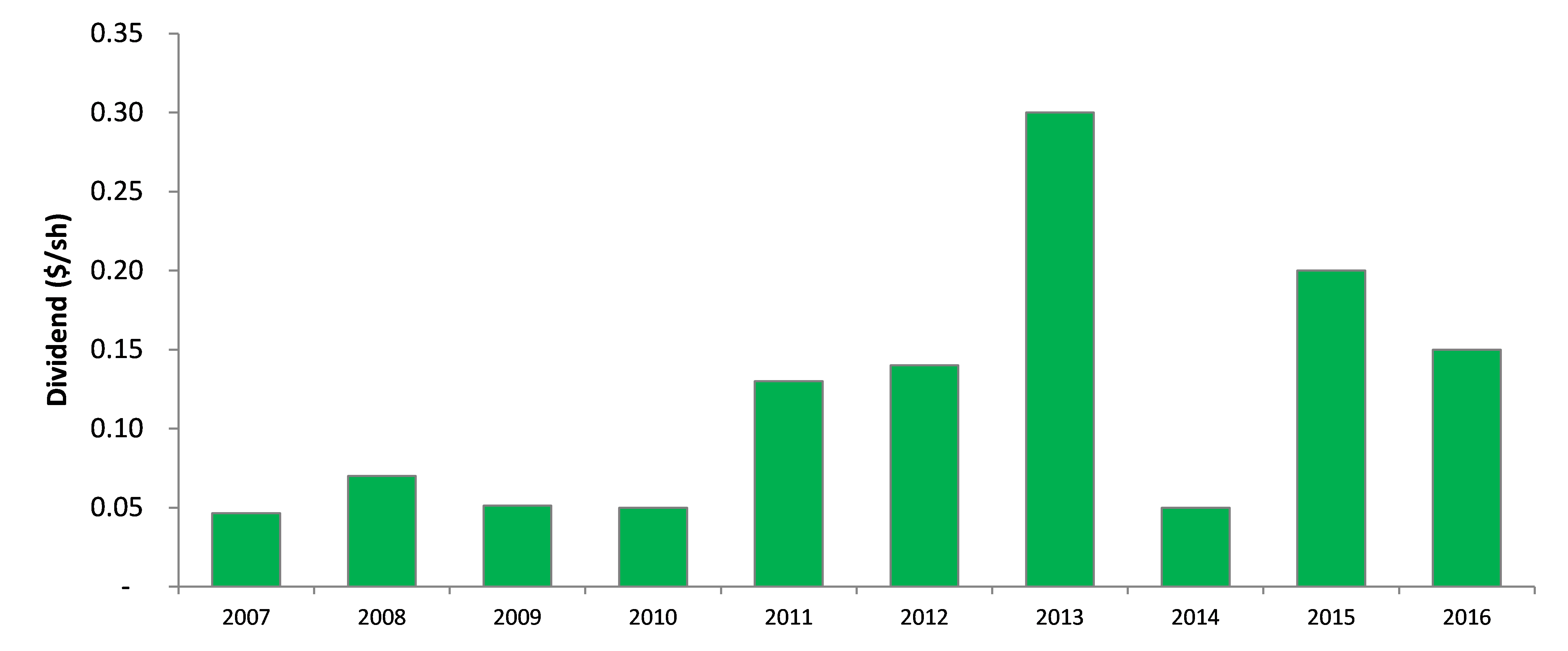

10-Year Dividend history: We calculated this using dividends paid from the cash flow statement divided by shares outstanding, due to timing of actual dividend payments it may not necessarily match exactly with other data sources. Bonal tends to issue dividends in $0.05/sh increments, even if the company continues to see weakness this year we expect they will still issue at least a $0.05/sh dividend, which would offer a 3% yield at current prices. While this dividend may need to be funded out of cash, the company does have $840K on hand, and the dividend burden at $0.05/sh is only about $90K so they would have no problem financing the dividend out of pocket for a period of time. In the brief financials the company provides, they do take pride in the longevity of their dividend history, which implies they are less willing to go a year without a payment.

Given the completion of spending on the new Meta-Lax device, we don’t expect other significant draws on cash flow. As a result, provided manufacturing activity picks up, we expect dividends will continue to be much higher than the $0.05/sh base.

Click to enlarge

Click to enlarge

Summary: Bonal has a great little business; even with an outdated product they are still able to dominate their niche. A newer product is on the way which uses the same base technology but should bring the equipment to the modern age. While growth opportunities for the company are small, we do see a path to a recovery in earnings from the weak last quarter, and along with it a path to 10%+ dividend yield, or more likely a higher stock price. Building a position in Bonal may prove challenging, but we expect using time as a catalyst will pay off.

Disclosure:I/we have no positions in any stocks mentioned, but may initiate a long position in BONL over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.