Adina Claici, Laurent Eymard and Shahin Vallée, The Brattle Group Inc and DGAP – German Council on Foreign Relations

This is an extract from the 2023 edition of the Europe, Middle East and Africa Antitrust Review. The whole publication is available here.

In summary

The decision to freeze the European economy to limit the spread of covid-19 demanded a strong public policy response to keep workers paid and companies afloat. The rapid suspension of European fiscal rules and the additional flexibility offered under state aid rules stimulated the adoption of national support programmes. However, these national emergency and recovery programmes differed in size, scope and instruments across the EU. In this context, this article aims at flagging certain issues that may require more scrutiny by policy makers in order to minimise the risks of distortions inherent to any public intervention.

Discussion points

- Summary of EU’s flexible application of state aid rules in response to the pandemic

- Medium- and long-term challenges presented to the single market by this relaxation

- Application of state aid rules to the EU recovery package

Referenced in this article

- The State Aid Temporary Framework

Introduction

The covid-19 pandemic, and the restrictions adopted to fight the spread of the virus, froze global economies for months. To limit the damage to livelihoods, governments around the world have responded with extraordinary measures to keep workers paid and companies afloat.

In Europe, despite the historical issuance of common debt by the European Commission, the policy response has, for the most part, remained national and has required that the rules that normally restrict national government actions be relaxed. In particular, the activation of the general escape clause of the Stability and Growth Pact, which suspended the application of European fiscal rules, and the adoption of the ‘Temporary framework for state aid measures to support the economy in the current covid-19 outbreak’ (the Temporary Framework), which clarified ex ante which aid measures would be compatible with European state aid rules, removed European constraints on sizeable national interventions.

Suspending fair weather rules against the backdrop of extraordinary circumstances was necessary; however, the adoption of covid-19 national support programmes that differed in size, scope and instruments has also increased the risk of competitive distortions within the European single market. As support measures become progressively more targeted at specific sectors and firms, we advocate for greater transparency and more stringent assessment of the trade-off between protection and distortions.

Covid-19 economic crisis

As the covid-19 virus spread worldwide, governments responded by locking down the economy to avoid further increases in the number of deaths. Although necessary, this decision had immediate and dramatic effects on production and income, and the EU economy contracted by 6 per cent in 2020 – the deepest recession since World War II.

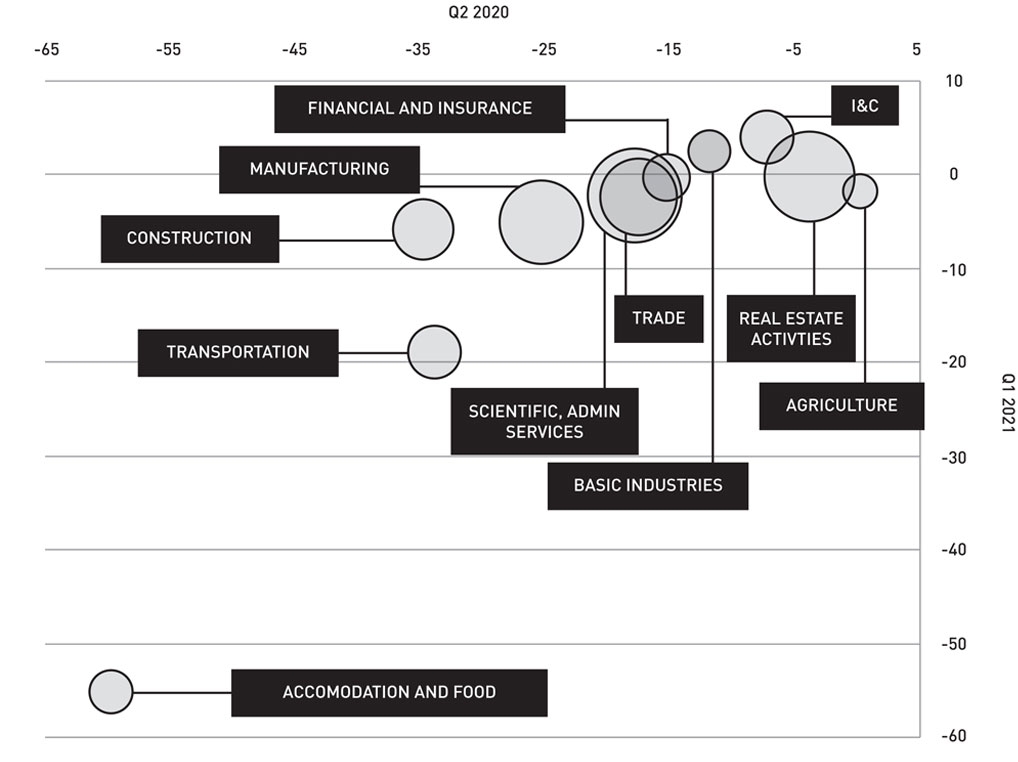

The economic effects of the covid-19 pandemic have varied across sectors, with hospitality and tourism being particularly affected by social distancing measures and travel restrictions. Figure 1 illustrates these differences by comparing levels of economic activity in France before and after the outbreak of the pandemic.

Figure 1: France – output loss by sector in Q2 2020 and Q1 2021 compared with pre-crisis (Q4 2019) levels

The horizontal axis shows that, by the end of the second quarter of 2020, economic activity in the hospitality, construction, transportation and manufacturing sectors was more than 20 per cent lower than before the crisis. By the end of the first quarter of 2021 (shown on the vertical axis), many sectors had already experienced a strong rebound; however, other sectors such as the transportation and hospitality industries are still suffering from a protracted contraction.

The magnitude and rapid propagation of the economic shock caused by the pandemic required expedited public intervention, which in the European Union could have been limited by state aid control procedures and fiscal rules. Mindful of this risk, the European Union quickly vowed to do ‘whatever is necessary to support Europeans and the European economy’, which in practice led to the first-ever activation of the general escape clause within the Stability and Growth Pact to relax budgetary rules that would normally apply under the European fiscal framework, as well as the adoption of the ‘most flexible state aid rules yet’ with the introduction of a temporary state aid framework.

EU state aid rules relaxed to allow timely policy response

Was it necessary to relax state aid rules? The response to that question is not as straightforward as it sounds. After all, the European Commission initially emphasised that ‘Member States [could] design ample support measures in line with existing state aid rules’.[6] Many of the support measures, such as wage subsidies, tax deferrals and direct support to households, are, for example, applicable to all undertakings and, therefore, do not qualify as state aid under article 107 of the Treaty on the Functioning of the European Union (TFEU).

But as governments contemplated using loan guarantees, various forms of subsidies and targeted aid, it quickly appeared that many if not most of those measures would fall under article 107 and would, thus, require approval from the European Commission.

Another option was to simply suspend state aid rules: several member states proposed that state aid rules be suspended for the duration of the fight against the covid-19 pandemic; however, the proposal was quickly dismissed.

It was decided to exploit the ‘full flexibility’ already enshrined in the TFEU. In particular, article 107(2)(b) authorises state aid that is granted ‘to make good the damage caused by . . . exceptional occurrences’ and article 107(3)(b) allows state aid that is granted ‘to remedy a serious disturbance in the economy of a Member State’.

On 19 March 2020, the European Commission further adopted the Temporary Framework, which clarified ex ante which aid measures were likely to be considered compatible under article 107 of the TFEU.

In normal times, assessing whether a state aid measure is compatible with the TFEU involves a detailed, case-by-case assessment of its necessity, incentive effect, proportionality and effect on trade and competition. Those detailed – and at times lengthy – assessments were clearly impossible in the context of the covid-19 pandemic; thus, the approach chosen was to specify minimum requirements in the Temporary Framework for a state aid measure to be cleared by the European Commission. Doing this removed the need for such detailed assessments and, thus, substantially accelerated the approval process for state aid.

What parts of member states’ rescue packages fall within the scope of state aid control?

In theory, both above the line (additional spending and tax cuts) and below the line (liquidity support, subsidised loans and equity injections) measures may fall within the scope of state aid control, provided that they meet the four criteria defining state aid in the meaning of article 107 of the TFEU. In practice, the bulk of measures related to the covid-19 pandemic that have a direct budgetary impact and were adopted in the first six months of the pandemic have fallen outside state aid rules, while guarantee (and subsidised loans) schemes were for the most part notified to the European Commission.

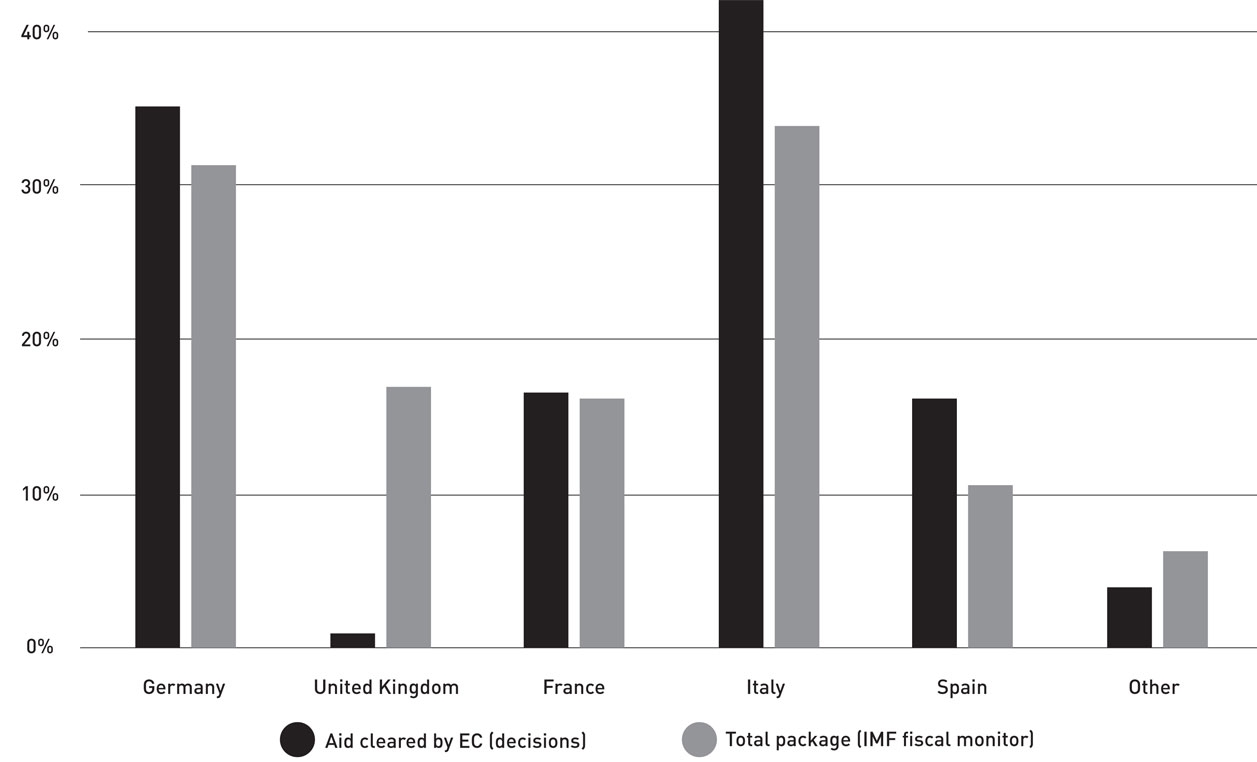

Figure 2 compares, for each of the European Union’s largest economies and the United Kingdom, the size of the off-budget liquidity support as summarised by the International Monetary Fund (IMF) with that of the loans, guarantees and recapitalisation schemes authorised by the European Commission. It shows that, with the notable exception of the United Kingdom, national liquidity support schemes have by and large been notified to and cleared by the European Commission.

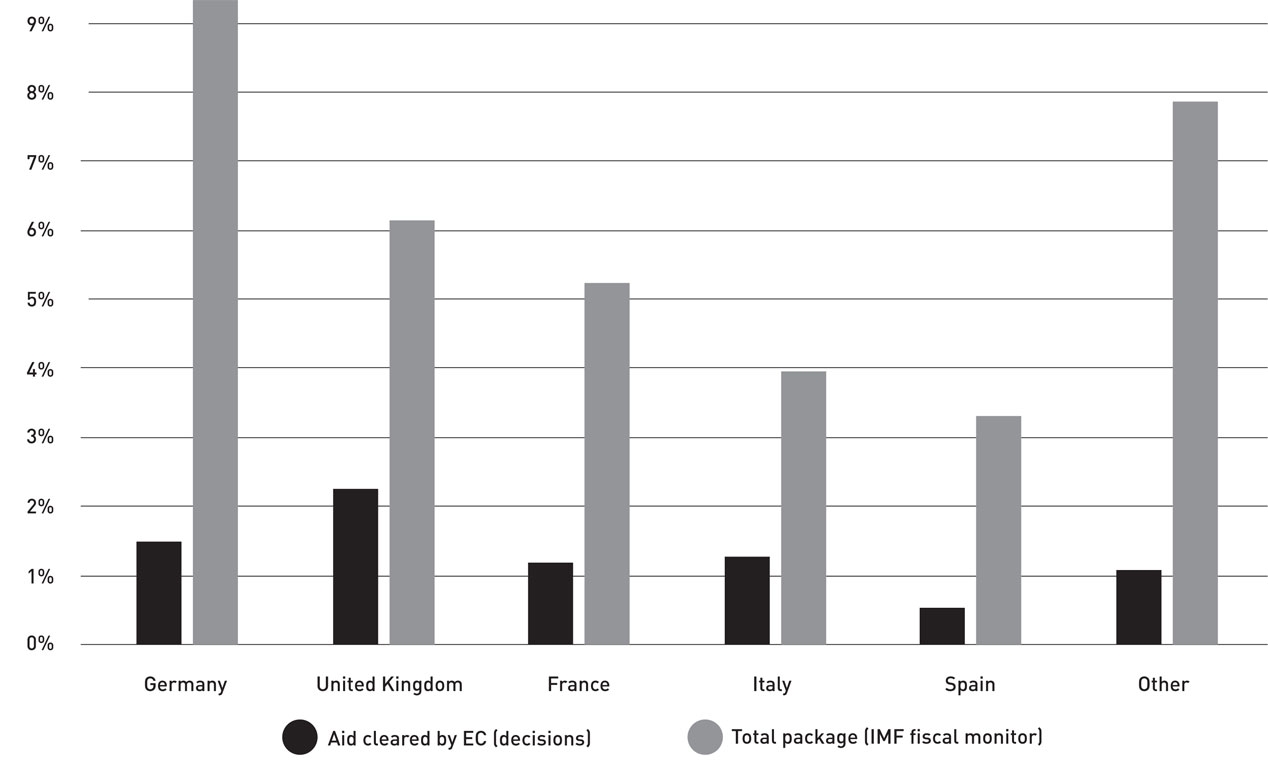

On the other hand, Figure 3 shows that only a small share of the budgetary measures introduced to cope with the crisis qualify as state aid in the meaning of article 107 of the TFEU and ended up being notified to the European Commission.

For example, for liquidity measures such as public guarantees, subsidised loans and support to trade credit insurance, the Temporary Framework required that a maximum amount per beneficiary be specified. When the Temporary Framework was extended on 3 April 2020 to include targeted aid to support the research, testing and production of covid-19-related products, the European Commission required that public support not exceed a certain share of eligible costs. For recapitalisation measures that became included in the Temporary Framework on 8 May 2020, the European Commission required minimum remuneration for public investments and restrictions on beneficiaries’ commercial expansion.

Figure 2: the bulk of liquidity schemes have been notified to the European Commission (% of 2019 GDP)

Figure 3: only a small share of above the line measures have been notified to the European Commission (% of 2019 GDP)

As at 30 September 2021, the European Commission has adopted more than 650 clearance decisions for aid related to the pandemic, totalling over €3 trillion in potential support to EU businesses. Massive rescue packages have been cleared with expedited review; while standard state aid reviews can take up to several months, it took the Commission just four working days to adopt a clearance decision on France’s €300 billion guarantee scheme[14] and just a weekend to clear Germany’s subsidised loans scheme.

The relaxation of state aid control is particularly evident in some clearance decisions, which are rather vague. The German subsidised loans scheme that was cleared on 22 March 2020, for example, does not specify a maximum budget.

The relaxation of control is also clear from the fact that national plans have, for the most part, been accepted without or with limited remedies or control over the actual distribution of the aid.

Relaxation of state aid rules raises challenges for single market

Assessing the compatibility of state aid with the TFEU is by nature a balancing exercise in which a measure’s positive effects are weighed against potential distortions of competition. There is little debate that public intervention was necessary following the outbreak of the pandemic and that it produced positive economic effects by softening the impact of an already devastating crisis; however, the compatibility of the massive aid packages cleared under the Temporary Framework raises important questions. With limited data on the actual distribution of aid measures published, it is hard to assess the degree of possible competitive distortions with precision.

Data on actual support is scarce and more transparency is required

In the first few weeks of the pandemic, a first wave of corporate support was introduced to cope with the liquidity crisis facing European businesses. In March 2020, Germany announced a massive extension of public guarantees for firms through the newly created Wirtschaftsstabilisierungsfonds (WSF) Economic Stabilisation Fund and the public development of the bank KfW. While it initially indicated that these would provide for up to €819.7 billion in guarantees (25 per cent GDP), Germany later clarified that the volume of federal guarantees would not be limited and could even exceed those already staggering figures.

Also in March 2020, the European Commission cleared France’s guarantee programme, which was designed to cover up to €300 billion in loans.

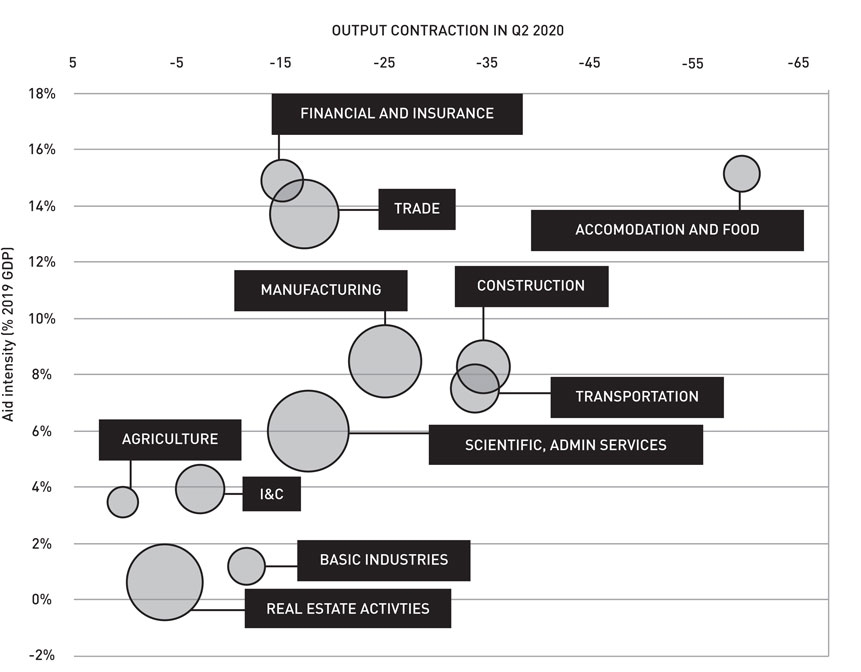

The relationship between output contraction and aid intensity

France publishes sectoral data on the actual allocation of guarantees by sector. As expected, the data reveal a strong link between the extent of the output collapse in a sector and the amount of credit support received (Figure 4); however, there appear to be some exceptions. Firms in the trade and finance and insurance sectors appear to have benefited, in relative terms, from a much greater level of support. Whether the surprisingly large amounts of credit support received by the trade, financial and insurance sectors were warranted is beyond the scope of this analysis. But establishing those patterns is a necessary first step in the monitoring of aid measures.

The headline envelopes of these guarantee schemes initially raised the concern that only member states with more fiscal space would be able to support their corporate sectors, putting firms in more indebted countries such as Italy at a disadvantage; however, by the end of April, other large European countries had completed their response packages with the deployment of similar public guarantee schemes aimed to support credit to firms (€565 billion in Italy, £331 billion in the United Kingdom and €129 billion in Spain).

Despite the apparent general character of these measures, distortions can arise in various forms, such as through the allocation of funds across sectors and firms. The clearance decisions provide limited information regarding how schemes’ beneficiaries are selected. Because the schemes are largely horizontal, covering all sectors (except financial services), actual distribution could be expected to be demand-determined and directed to sectors that suffered the hardest blows.

However, the disbursement of the funds is subject to numerous trade-offs, and one cannot rule out that the allocation of credit is also used strategically to support certain industries or to favour specific companies. Only granular data can help in observing the concrete implementation of the support schemes.

Section 4 of the Temporary Framework provides that member states have an obligation to publish comprehensive data on individual aid above certain thresholds on a dedicated website; however, most member states have yet to comply with this obligation. Even aggregated data on actual usage numbers can be difficult to obtain, with France being the only country where a breakdown is provided at the sectoral level.

To assess the risk of long-term competitive distortions, greater transparency is needed. Clearly, there is scope for the European Commission to tighten and harmonise reporting requirements. Data on the role played by national development banks and commercial banks in allocating covid-19 credit support should also be provided.

Figure 4: output contraction and aid intensity by sector in France

Targeted aid, risk of subsidy race and temptation of helping national champions

As part of the third amendment to the Temporary Framework, the European Commission introduced a provision that explicitly forbids that aid ‘be conditioned on the relocation of a production activity or of another activity of the beneficiary from another country within the EEA to the territory of the Member State granting the aid’; however, several packages appear to display such features according to their presentation by public officials.

For example, the €5 billion of government loan guarantees for the automobile manufacturer Renault was conditioned on limiting the number of factory closures in France. Finance Minister Bruno Le Maire explicitly stated that the reshoring of the production of electric and hydrogen-fuelled vehicles and batteries was a condition for accessing help under the government’s automobile plan. Beneficiaries of the €15 billion aerospace plan were also required to think about ways to bring production and strategic, technological know-how back to France.

The case of Lufthansa’s €9 billion support package illustrates another way state aid can be used to promote domestic economic interests at the expense of foreign economic interests. In that case, the issue was not that the aid was conditioned on repatriating production, but the sheer size of the package – even Lufthansa’s own CEO, Carsten Spohr, admitted that the total envelope was more than what was strictly necessary to deal with the losses associated with the crisis and instead reflected the government’s desire to reinforce Lufthansa’s ‘global leading position’.

Yet Germany’s support package to Lufthansa was cleared under the Temporary Framework. And while the Commission took the extraordinary step to impose structural remedies in the context of a state aid case, those remedies appear, at first glance, to be relatively mild in light of the risk of competitive distortion.

In terms of their compatibility with the single markets, targeted covid-19 aid raises two main issues:

- Proportionality of the rescue measures: under normal circumstances, aid measures that go beyond what is strictly necessary to achieve the objective pursued (which in this case is to alleviate the effect of the covid-19 pandemic) would not meet the criteria of proportionality and would be considered as incompatible with the common market. In the current context, conducting such a proportionality assessment would require disentangling the effect of the pandemic from that of other factors; however, such detailed assessment is not always conducted for measures notified under the Temporary Framework, and it is unclear whether the safeguards included in the Temporary Framework (in the form of maximum aid amount, loan and guarantee maturity, etc) are enough to ensure that aid measures are proportionate.

- Effect on competition: the effects that a given aid measure may have on competition are often difficult to predict ex ante, even in normal times. In the context of a global pandemic, these difficulties are compounded by the significant uncertainty regarding what would have happened absent the aid (the ‘counterfactual’ scenario, the definition of which is an essential part of the Commission’s assessment). In addition, the effect of a given measure may not be analysed in isolation as the various components of member states’ rescue packages (including measures that do not constitute state aid in the meaning of article 107 of the TFEU) may complement and reinforce one another.

State aid and recovery packages

The Temporary Framework, including its numerous updates, has enabled the Commission in a relatively short period to assess and approve a vast number of state aid applications aimed at supporting European economies to navigate the health crisis. As the Temporary Framework is set to expire in 2022, attention is now shifting to recovery. In 2020, the European Union agreed to an unprecedented stimulus package worth €2.018 trillion. It comprises the European Union’s long-term budget for 2021 to 2027 of €1.211 trillion, topped up by €806.9 billion through NextGenerationEU, a temporary instrument to power the recovery.

The centrepiece of NextGenerationEU is the Recovery and Resilience Facility (RRF), which is an agreement that paves the way for providing grants and loans to support reforms and investments in the EU member states. To finance NextGenerationEU, the European Commission will borrow funds on the capital markets, and those funds will be distributed according to national recovery and resilience plans prepared by each member state, working in cooperation with the European Commission.

The assessment of those plans is governed by the RRF Regulation. Article 3 of the Regulation lists the policy areas of European relevance that can benefit from support:

- green transition;

- digital transformation;

- smart, sustainable and inclusive growth;

- social and territorial cohesion;

- health, and economic, social and institutional resilience; and

- policies for the next generation, children and the youth.

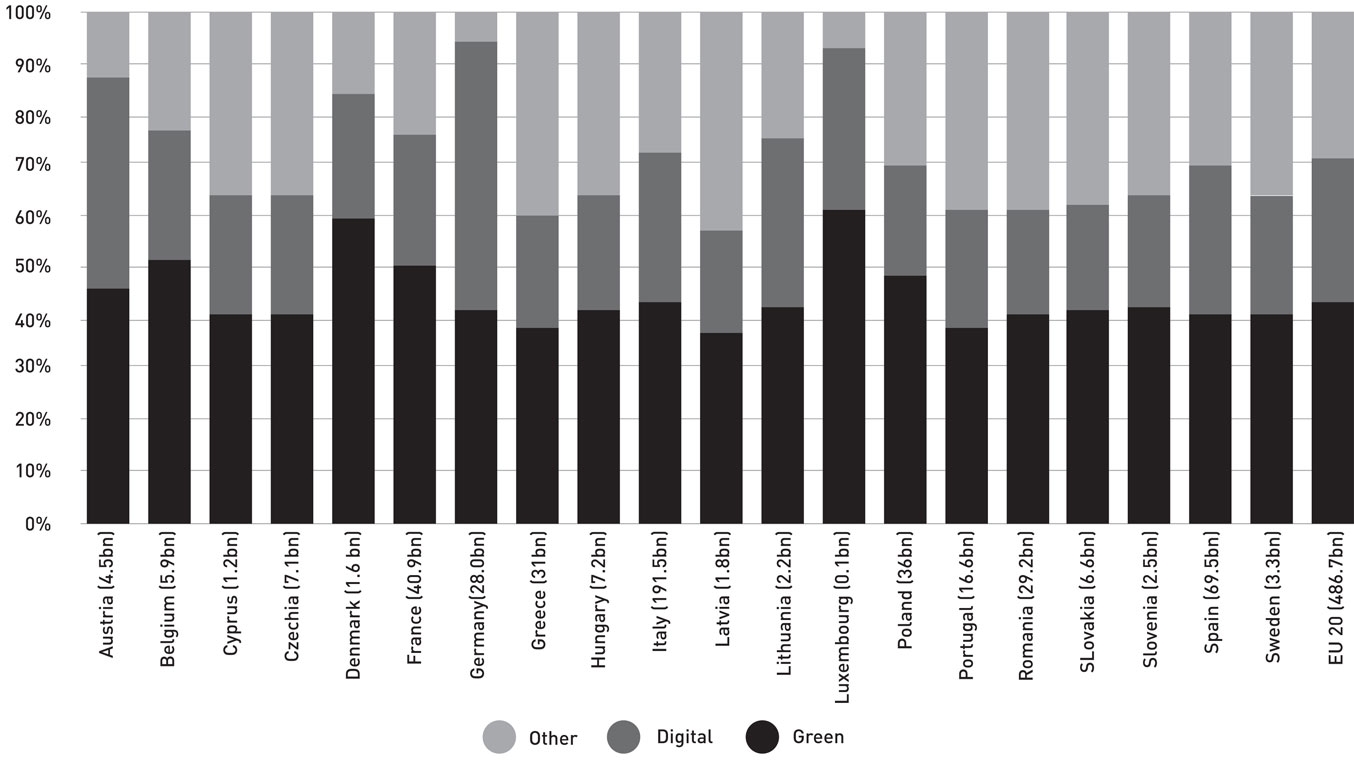

Each member state’s recovery and resilience plans must allocate at least 37 per cent of expenditures to support the green transition, and at least 20 per cent must go towards digital transformation. As at October 2021, those targets have been significantly exceeded in the plans approved for 20 European Union member states.

Figure 5: overall resource allocation in natural recovery and resilience plans (% of total and € billions)

In essence, the recovery from the covid-19 pandemic is being used as a vehicle to boost European political priorities for the future. Since the funds will be channelled through member states’ budgets and partially earmarked to specific sectors, part of the spending will qualify as state aid under the TFEU.

To the extent that this is the case, there is a risk that RRF funds could fuel a subsidy race and competitive distortions, which state aid rules are precisely there to avoid. Whether this should be of concern, however, depends on the objective that the aid measures adopted under the plan are pursuing.

When the funds are spent for social purposes (eg, in the case of four of the RRF’s six policy areas), they normally benefit consumers and broader society in a direct way, with the sole concern of cost efficiency to avoid a waste of resources; however, when the purpose of the funds is to boost some economic activities in certain areas (eg, in the case of the RRF’s objectives related to the green transition and digital transformation), there is a potential to interfere with market function. In this case, it is important to define the clear purpose of the support. In principle, it could be either to correct a market failure or to push market boundaries as a form of industrial policy.

In the case of the green transition, there are standard externalities, and the EU Guidelines on State aid for environmental protection and energy have already been in place for a long time to correct this market failure. Currently, given the ambitious goals of the Commission stated in the Green Deal initiative, the RRF may be well placed to complement the efforts made by member states in that direction.

In the case of digital transformation, the purpose of the public boost is less straightforward. According to the Commission, digital transformation includes investments in supercomputing, artificial intelligence, cybersecurity, advanced digital skills and the wider use of digital technologies across the economy and society. It will be interesting to see why European markets cannot deliver those assets without public support or if they can only deliver them at a level that is considered socially sub-optimal.

In that context, a counterfactual analysis – as with any other competition policy area – could establish the status quo without support (current and forecasted), as well as the various outcomes that public support could achieve. Such an analysis may ensure an efficient use of resources, similar to the proportionality test performed in state aid assessment.

A very preliminary comparative look into those two sectors may seem to suggest that the probability of costs (competitive distortions) outweighing the benefits of support (addressing a market failure) would appear more important in digital, where there’s a greater risk of crowding out private investment. This should lead to greater scrutiny of aid measures.

We believe that the way the RRF was set may provide a good way towards achieving the desired policies with the minimum resources necessary. In particular, after performing an ex ante assessment of the national plans and approving the overall amounts, the European Commission will disburse the funds in batches, conditional on the achievement of the agreed milestones and targets. A sound counterfactual analysis performed by member states may enable the Commission to check periodically if the spending is on track or if it deviates considerably from the desired outcomes, in which case corrections may be necessary.

Conclusion

The covid-19 pandemic and public intervention to limit its economic impact represent a challenge for economic policy in general and for state aid control in particular. Policymakers are faced with the difficult need to meet short-term objectives by allowing generous and expedited rescue packages while ensuring longer-term objectives, such as maintaining the level playing field in the single market or economic convergence across the European Union.

The Commission should be commended for its swift reaction to the pandemic, which made it possible for governments to deploy the full force of their policy instruments to address the unprecedented macroeconomic challenges of the pandemic. Enforcement of state aid rules has been adapted so that it would not stand in the way; however, concerns about the single market are growing as it appears evident that member states are unevenly able to deploy rescue instruments (owing to limited fiscal space and a lack of tools, such as national promotional banks) and that policy is becoming more and more targeted to support individual companies or sectors.

The European Union has not remained silent in addressing those challenges. It has decided to raise funds on the capital market that will subsequently be channelled to individual member states in the process of recovery from the crisis.

Notwithstanding the advantages of such a centralised approached, the European Union should be careful not to fuel a subsidy race between member states with EU funds. A strict requirement of monitoring and reporting may ensure transparency in the member states’ expenditures. Such transparency may be a first step in controlling and limiting the inherent distortions in competition and trade.

*The authors are grateful to Paul May and Lilian Pouget for research assistance. The authors also thank Julia Anderson for useful conversations. The views expressed here are those of the authors alone and do not represent their respective places of work.

Subscribe here for related content, breaking news and market analysis from Global Competition Review.

Global Competition Review covers the most crucial developments in competition law and enforcement worldwide with breaking news commentary and analysis five days a week, as well as original in-depth reports, interviews and features on antitrust enforcement worldwide.