NEW YORK (July 26) – Gross Domestic Product (GDP) growth for the second quarter of 2019, or “2019Q2”, printed at 2.1%, above the consensus estimate of 1.8%. That’s 100 bps below the final 3.1% reading of the last quarter and also 1.4 percentage points below the comparable period last year.

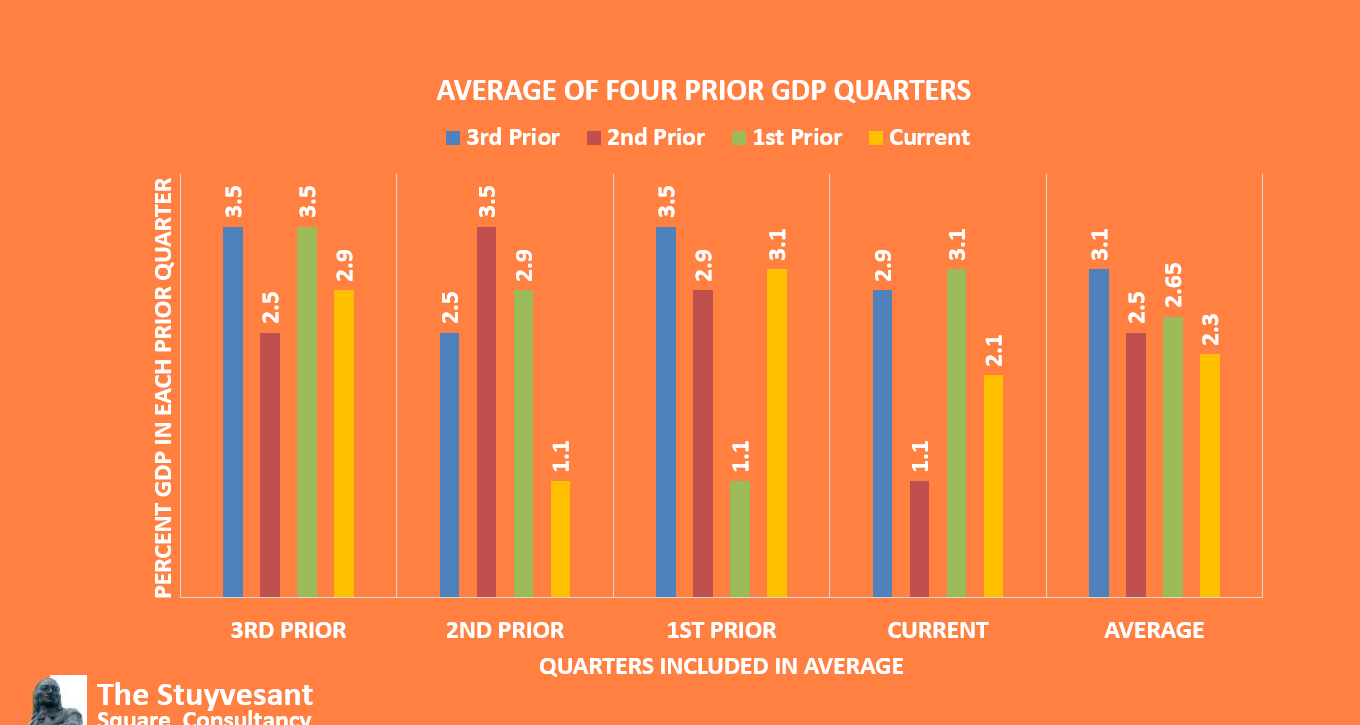

Average GDP growth for the last four quarters printed at 2.3%. That compares to average GDP growth for the prior four quarters (2017Q3 to 2018Q2) of 3.2%. It is the lowest average of the four-quarter GDP print since 2017Q2.

The 2.1% GDP growth rate was almost midway in line with our last jobs report, where we had anticipated growth in 2019Q2 to print at between 1.9% and 2.4% slightly above the consensus.

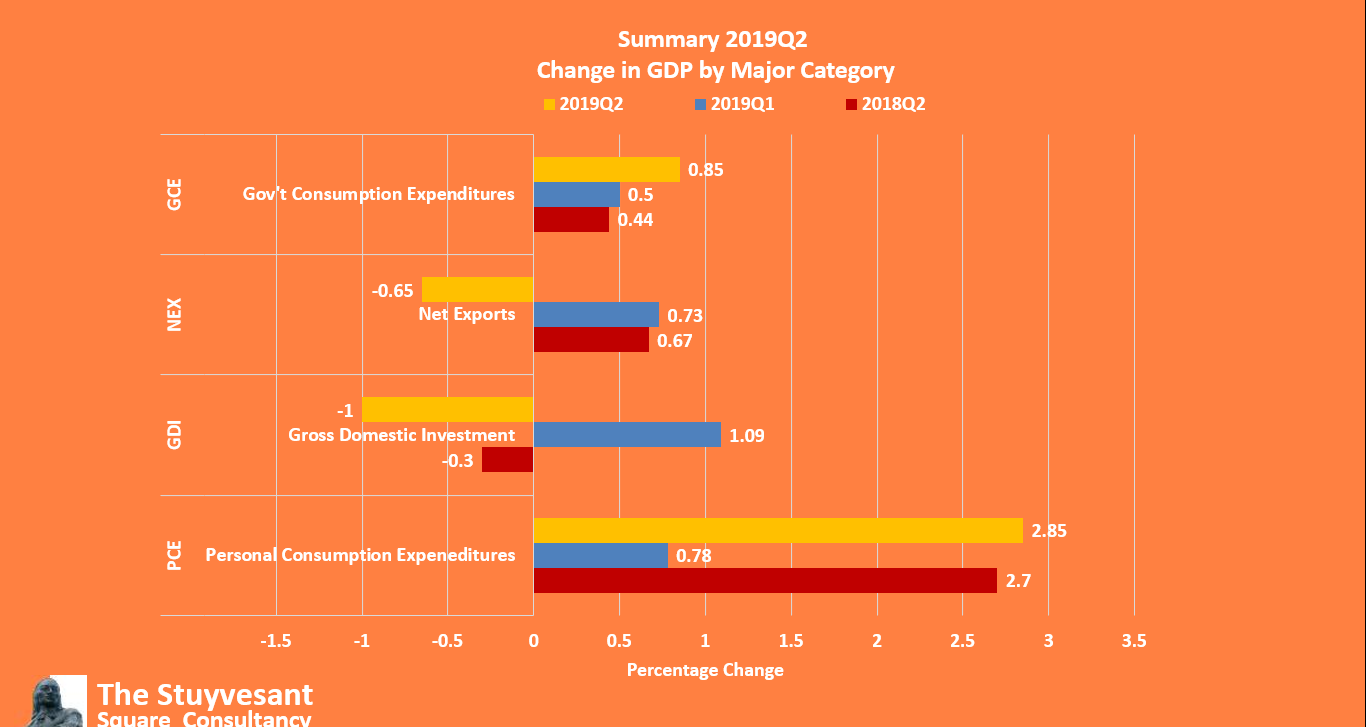

The 2019Q2 GDP was led by Personal Consumption Expenditures, or “PCE”, which printed at 2.85%. The weakest of the four GDP components was Gross Domestic Investment, “GDI”, which was cut by 100 basis points. That was followed by Net Exports, or “NEX”, which was reduced by 85 bps.

A Slew Of Timing Differences

2019Q2 is characterized by the effect of timing differences between major categories of GDP, principally NEX and Gross Domestic Investment, “GDI”, as illustrated here: .Components of 2019 Q2GDP

.Components of 2019 Q2GDP

The NEX reduction follows the more than 100bps addition NEX contributed to 2019Q1. We had warned in our report for that quarter that 2019Q2 would not repeat, but the numbers came in worse than we anticipated. The 2019Q1 NEX had been substantially higher than other quarters in recent years.

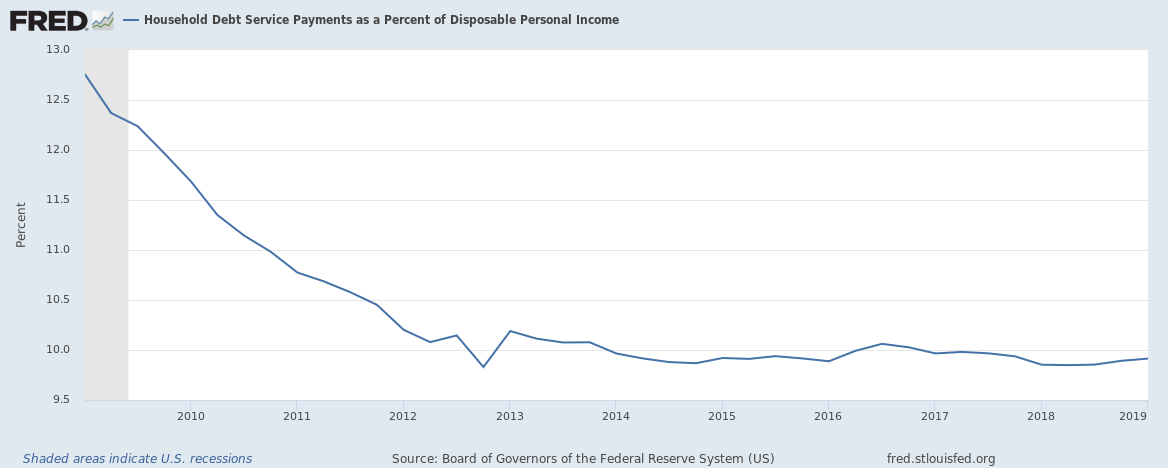

Similarly, GDI reduced in the second quarter as inventories built up in 2019Q1 were substantially reduced. Even Personal Consumption Expenditures, “PCE,” this quarter has a timing difference from the low level in 2019Q1. (We had anticipated PCE to grow in the range of 1.2% to 1.7% throughout all of 2019 and be a bigger contributor to the economy, but the precipitous dip in consumer confidence during the government shutdown (12/22/2018 to 1/22/2019) likely affected the first month of the 2109Q1 PCE). Nevertheless, we anticipate that PCE will continue to “muscle through” at least 2019Q3 and even possibly Q4, as the IBD/TIPP Economic Optimism Index for July climbed to 56.6, following a big drop in June. Debt service as a percentage of disposable income is at among its lowest levels in a decade (see chart) and durable goods orders and real PCE spending are both up.

Summary Analysis

As stated, 2019Q2 GDP came in at the midpoint of what we anticipated. But we continue our concerns with inter-quarter volatility. Huge swings in quarter-to-quarter results may produce acceptable quarter-to-quarter GDP results, but we note that in the average of the last four quarters over the last year, the 2.3% average GDP for the four quarters ending in 2019Q2 is the lowest of the four prior quarter GDP averages, as shown here:

Short Term

Based on all we see, we expect 2019Q3 to print in the range of 1.7% to 2.2%. But watch for our monthly jobs reports, where we go through multiple data points, for revisions up or down on that number. As stated, the IBD/TIPP index of Economic Optimism for July jumped 6.4 points to 56.6. The other IBD/TIPP economic indexes, which are based upon surveys by TechnoMetrica Market Intelligence, are similarly optimistic. That outlook is supported by strong consumer sales and consumer durables orders.

We continued to be troubled by volatility, flattening and inversion in the 3Mo/10Yr yield curve, which has been narrowing on and off since the end of 2017 and inverting in recent months. On July 3rd, the 3Mo/10Yr inverted by 25 bps.

While many of these inversions are attributable to what we view as a mistaken rate increase by the Fed in December of 2018, much of it is also likely due to the influx of foreign capital avoiding negative interest rates in much of the rest of the OECD. Nevertheless, we view the anticipated rate cut next week as supportable only if the Fed acknowledges its December error. It seems to us that Chairman Powell is searching for some basis (the slowing global economy, the trade war, etc.) for a rate cut simply to ameliorate the impact of his December rate cut error. We would prefer he simply acknowledge the error instead of talking down an economy that is, given the circumstances, performing reasonably well, with average four-quarter growth at 2.3% and unemployment at 3.7%. In fact, we would prefer the Fed not increase rates because of the recent trimmed mean core inflation numbers in April (3%) and May (2.3%). Until we can be assured inflation is not cropping upward beyond the 2% target, we would prefer the Fed to “stand pat”, notwithstanding its signals to the contrary. M2 velocity remains fairly flat. If the Fed reduces rates further, we anticipate this will remain flat or even a further decline.

Medium Term

We remain somewhat pessimistic over the medium term because we see recent distinct signs of a slowing economy, particularly in housing starts and home sales, and the volatility in the individual GDP components.

Inflation remains low, seemingly inapposite to the dogma of the Phillips Curve. Likewise, a low interest rate environment and a low M2 velocity in a medium-growth economy seem contrary to the Quantity Theory of Money (MV=PQ, sometimes written as MV=PT). We’re of the view that both of these rules are affected – and possibly made obsolete by – the Fed now paying interest on excess reserves, something it had not done prior to 2008. This is because so much of the money produced by Fed Open Market Committee operations is being kept in the banking system, at the Fed, instead of in the regular economy. We’ve never had that before; some older economic theorems may now be consigned to the dustbin.

Notably, Judy Shelton, President Trump’s nominee to the Fed, has called for the Fed to return one of the tools it used during the financial crisis, paying interest on Fed member banks’ excess deposits, to the toolbox. We agree and think that such a step – or at least differentiating the excess deposit rate with a lower rate from the regular deposit rate – is a far better means of improving liquidity and reversing the yield curve inversion than reducing rates.

Long Term

Our long-term view of the economy, beyond 2022Q1, remains unchanged.

Aside from AI, 5G, and electric cars – none of which are fully “ripe” to make a significant impact on the economy – there is really very little in this economy we see on the horizon to create rapid, robust, and continuing growth; that is, the “next big thing” in the way of a product or service that ramps up a sustained, substantial uptick in production and consumption to drive growth.

What growth there is now is largely coming from what we call soft-sectors: personal services like food and product delivery and on-demand taxi and cable TV services; social media; and consumer non-durables. Meanwhile, big industrial firms like Boeing (NYSE:BA) and Caterpillar (NYSE:CAT) – where thousands of people are employed and wages tend to be high – are struggling with technological issues and trade.

President Trump’s more protectionist trade rhetoric could add foreign-owned domestic production to drive GDP growth, particularly in the GDI category. But, so far, that rhetoric has mostly been a threat to induce more fair trade policies from our trading partners. Much remains to be seen.

Direct foreign investment in the USA has started to ramp up in the last few quarters, notwithstanding trade issues. We anticipate that ratifying the United States-Mexico-Canada Agreement, the “USMCA, will add a couple of basis points to GDI as will a favorable resolution of the China trade talks. Nevertheless, barring some CPE growth from some major consumer-oriented innovation (perhaps 5-G, which would add to both PCE for consumer and GDI for its infrastructure), or some more significant reshoring of manufacturing or other direct foreign investment in the USA, we anticipate managers will look for growth in certain low-margin industries and to acquire and consolidate competitors to realize cost savings from economies of scale. We also expect internet retailers, like Amazon (NASDAQ:AMZN), to realize enhanced growth by adding to their business of selling “stuff” to their nascent business of selling “experiences” – concert tickets, airlines, cruise lines, car rentals, theme parks, hotel chains, etc.

Investment Summary

In equities, we’re mostly inclined to stand pat with these sectors from our June jobs summary, with some changes, as follows:

-

Outperform: Consumer discretionaries across all sectors; trucking and delivery services on speculation of consolidation and acquisition; companies or REITs that own real estate in sectors identified as “opportunity zones” under the Tax Cut and Jobs Creation Act of 2017; and CHF.

-

Perform: Consumer staples, energy, utilities, telecom, and materials and industrials; the asset-light hospitality sector on speculation of stabilizing franchisee property values and room rental costs; certain leisure and hospitality; and healthcare.

-

Underperform: Financials; and technology; lower-end, low-quality QSRs (e.g., MCD, DPZ, YUM, etc.) on greater US delivery competition and a slowing economy; lower end hospitality on gasoline prices; currencies of developing nations, such as INR; and the GBP and EUR.

______________________________________________

Author’s Note: Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients. Others discuss new management strategies we believe will fail. This approach lends special value to contrarian investors to uncover potential opportunities in companies that are otherwise in downturn. (Opinions with respect to such companies here, however, assume the company will not change). If you like our perspective, please consider following us by clicking the “Follow” link above.

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: The views expressed, including the outcome of future events, are the opinions of the firm and its management and do not represent, and should not be considered to be, investment advice. You should not use this article for that purpose. This article includes forward looking statements as to future events that may or may not develop as the writer opines. Before making any investment decision you should consult your own investment, business, legal, tax, and financial advisers.