Can an increase in automation on the factory floor also translate into more jobs?

Photographer: Charly Triballeau/AFP

Photographer: Charly Triballeau/AFP

To get Brooke Sutherland’s newsletter delivered directly to your inbox, sign up here.

The coronavirus pandemic spawned all kinds of predictions in March and April that now look a bit overdone in September: Cities aren’t dead (yet), commercial office buildings aren’t relics (yet) and we will likely board planes again for both vacation and business (although the frequency of this is still up for debate). But one area where long-lasting change is already underway is in supply chains.

We talked last week about a Bank of America Corp. survey that found a growing number of manufacturers were looking to “widen the scope” of plans to relocate, or reshore, factory work closer to where products are actually bought and used. That wording is telling: this isn’t a new idea. The Covid-19 shock to cities, real estate and aviation was impossible to predict in January, much less a year ago, but the risks embedded in far-flung parts networks have been growing increasingly apparent for a while now. “While disruptions from the pandemic might have acted as a catalyst to accelerate reshoring, we believe that the underlying structural reasons are grounded in an ongoing shift to ‘stakeholder capitalism’ where corporations focus on shareholders’ interests, as well as the broader community of consumers, employees and the state,” the Bank of America researchers said. In other words, the pandemic is just adding a lot of grease to wheels that were already in motion for various other reasons, including the U.S-China trade war and the growing importance of environmental, social and governance initiatives.

Indeed, electrical and automation-equipment company Schneider Electric SE was already focused on shortening its own parts networks as part of a commitment to reduce its carbon footprint, Ken Engel, senior vice president of global supply chain in North America, said in an interview this month. Schneider is still a global company with a global supply chain, but the logistical logjams caused by the pandemic have made it more imperative for both the company and its customers to build in more resilience and consider localizing certain kinds of manufacturing work, Engel said. Schneider actually purchased face-mask machines for facilities in North America, Europe and Asia to make sure it could protect its workers, Engel said. The “just-in-time” mindset that kept inventories as lean as possible and arbitraged labor costs across wide-reaching parts networks is being replaced by “just-in-case” planning for factory disruptions or emergency surges in demand. Backup vendors are becoming more important for even lower levels of the supply chain, Engel said, and that includes lining up capacity in multiple geographies.

Schneider feels like it’s ahead of the curve, though, thanks to pre-existing investments in digital tools like automation and software, Engel said.

I took a virtual tour this week of Schneider’s Lexington, Kentucky “smart factory” that manufactures electrical load centers and safety switches. I was struck foremost by the scarcity of humans on the factory floor. The other fascinating thing was how smoothly older automation systems that had been in place for 20-plus years were melded with newer robotic technology and software systems. Schneider’s EcoStruxure industrial software is designed to be standardized enough to be easily implemented and scaled, while adaptable enough to meet individual customers’ needs; the analytics platform sold by partner Aveva Group Plc integrates all the different data points and allows plant managers to look at the old and new parts of the factory as an entire ecosystem. That means customers don’t need to retool a factory from scratch to get productivity and energy savings. Schneider’s power monitoring software has helped put the 62-year old Lexington facility on track to reduce its energy consumption by 11% in 2020, while augmented reality tools have helped reduce the mean time it takes to repair equipment by 20%, says controls and manufacturing engineering manager Jeremy Elias.

These kind of innovations may serve as a blueprint for others as manufacturers think about how to shift production away from China without significantly ratcheting up their operating costs. The Lexington facility makes 70% to 80% of the parts needed for its products in-house, a level of vertical integration that’s rare these days, says plant manager Steve Lyczkowski. The automation benefits are so great that the plant actually ships some parts to Mexico, a flip on a narrative that usually runs the other way.

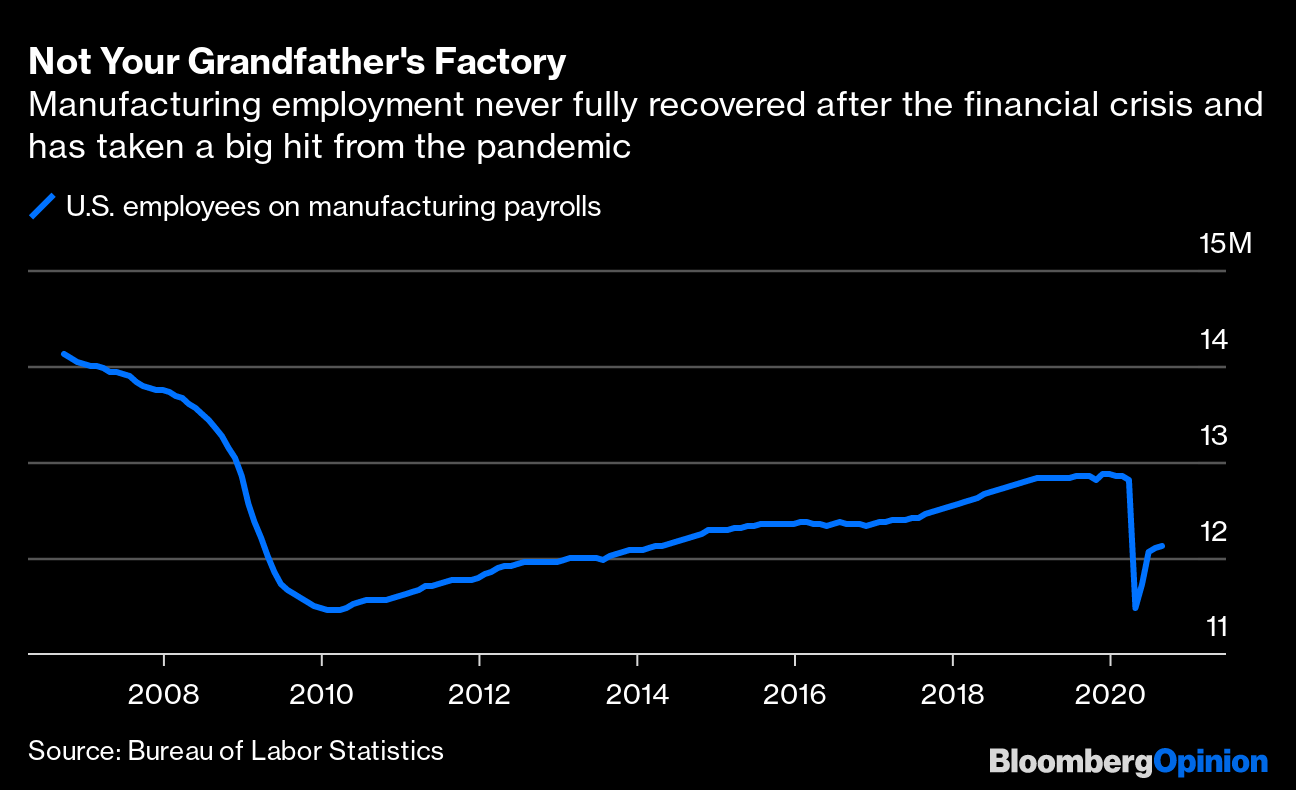

Not Your Grandfather’s Factory

Manufacturing employment never fully recovered after the financial crisis and has taken a big hit from the pandemic

Source: Bureau of Labor Statistics

All of this automation raises the uncomfortable question of how any post-pandemic resurgence in North American manufacturing translates into jobs. Employment data released on Friday showed the manufacturing labor force grew by 29,000 in August, less than half the median estimate of economists. Overall employment for the sector is still more than 700,000 jobs short of February levels.

Remember the dearth of people I mentioned in the Schneider’s Lexington facility? There are actually some 400 workers on a typical day, with around 350 manufacturing employees working three shifts and some 50 salaried employees, Lyczkowski said. That’s a reduction from the workforce of years past, but the increase in automation clearly hasn’t wiped out the need for humans altogether. The jobs are just different. The idea behind this digital push is to get more out of the machines but that also means getting more out of the employees. Schneider needs laborers with the skills to work with industrial software systems and pivot between different jobs and product responsibilities. Whereas before, an assembly line might be used for one product, it can now be adapted to a mix of six or eight products; a press operator who previously ran one machine might now be in charge of four. “There are issues with finding that kind of talent sometimes,” Elias said.

A shortage of skilled labor means some companies are turning to digitization merely as a means of maintaining the status quo as workers retire and take their operating and maintenance knowledge with them, says Saar Yoskovitz, CEO of digital machine-health company Augury. “It’s not about replacing jobs,” he said. Companies are “having a hard time just staying in place. How do we double the manufacturing capacity in the U.S. if we don’t have enough people?”

The Trump administration’s approach to encouraging more domestic manufacturing has been a combination of carrots (tax breaks and government contracts) and sticks (trade wars and public pressure) — with some success. His Democratic challenger, former Vice President Joe Biden, is proposing a $300 billion investment in research initiatives and a $400 billion push in government procurement of American goods, while closing loopholes that allow foreign entities to benefit from such programs. Giving manufacturers even more incentive to build things in the U.S. is a good start, but both approaches leave a significant gap when it comes to educating the workforce for the jobs that will be created as a result of this push.

DEALS, ACTIVISTS AND CORPORATE GOVERNANCE

Fortive Corp. this week laid out an updated plan for the separation of its Vontier Corp. business, a collection of transportation products ranging from gas-station fuel pumps to traffic and fleet management systems. Fortive had put the split on ice in April as the pandemic roiled markets, but it now expects to complete the divestiture by the end of the year. Just over 80% of the Vontier business will be spun off to existing Fortive shareholders, while the parent company will retain a 19.9% stake that it intends to divest in a tax-efficient manner over the course of the first year following the separation. Vontier will make a $1.6 billion cash distribution back to the parent company, funded with new debt. This is a different structure than Fortive had previously proposed; its initial plan called for a split-off transaction where about 20% of the Vontier business would be taken public and existing Fortive investors would have to opt in to exchange their shares for an 80% stake in the new company, rather than just receiving shares automatically through the spinoff format. This would have allowed Fortive to collect more cash upfront and avoid the risk of forced selling by investors who can’t or don’t want to own the new company. But the spinoff route is easier to execute and gives Fortive a more straightforward path to cash out twice on the same asset in an uncertain macroeconomic environment. Either way, it’s just nice to have some certainty and Fortive shares rallied on the news.

Danaher Corp. was sued by the pension fund of Pontiac, Michigan, over the lack of diversity on its board. The City of Pontiac General Employees’ Retirement System, which oversees funds for a predominantly Black suburb of Detroit, claims the lack of Black directors at Danaher amounts to a breach of its fiduciary responsibility. It bases this in part on a 2015 McKinsey & Co. study that shows companies with more diverse leadership teams tend to outperform. It’s an interesting argument from a shareholder at a time when issues of racial justice and equality are front and center in America. More companies are apt to come under this kind of scrutiny in the coming months; about a dozen of the largest companies by market value in the S&P 500 Index have no Black board members, according to data gathered by Bloomberg News. The Pontiac pension fund is reportedly seeking damages on the part of individual directors and asking Danaher to add three minority board members and remove any institutional hurdles to diversity initiatives.

Gogo Inc. agreed to sell its in-flight connectivity business to bankrupt satellite operator Intelsat SA for $400 million. The idea is to help Intelsat further expand beyond a faltering satellite television and media business into the consumer-facing side of in-flight entertainment. While not many of us are taking flights today, Intelsat is betting we will still want access to movies, games and news when we eventually board planes again. It may even become more important to the airlines to offer free, reliable WiFi as a way of differentiating themselves in a prolonged recovery in air travel. Already, United Airlines Holdings Inc.’s decision to do away with change fees on full-price tickets prompted a quick response from Delta Air Lines Inc. and American Airlines Group Inc. Intelsat CEO Stephen Spengler said the company’s ability to execute the transaction in the middle of bankruptcy restructuring “speaks to the strength of our underlying business,” which I suppose is one way of putting it. Another way is that it’s hard to find a more apt peak for irrational exuberance than a still-bankrupt company using debtor-in-possession financing to do a deal. None of this is Gogo’s problem, though. The commercial aviation division has been a drain on cash flow and the new Gogo will consist of a highly profitable business-aviation unit with strong market share. Analysts called the deal “transformative.”

Schlumberger agreed to sell its North American fracking business — known as OneStim — to Liberty Oilfield Services Inc. The all-stock transaction will give Schlumberger a 37% stake in the smaller operator, valued at about $448 million. It’s just the latest exit by a major oilfield-services company from a shale-related market that was once a hot spot for investing but has become increasingly less attractive amid a prolonged slump in crude prices and investor demands for more disciplined spending. OneStim helps customers extract oil and gas from shale wells by blasting water, sand and chemicals underground to release trapped hydrocarbons. Schlumberger paid $430 million for Weatherford International Plc’s fracking unit in 2017, among other shale-related deals. Liberty said Tuesday it would permanently retire capacity equivalent to 1 million horsepower — effectively the Weatherford fleet — from the market amid weak demand.

Kansas City Southern officially received a takeover offer from private equity firms Blackstone Group Inc. and Global Infrastructure Partners, a person familiar with the matter told Bloomberg News. Terms of the offer aren’t known, but the Wall Street Journal reported that Kansas City Southern has already rebuffed one bid from the buyout group. As I wrote earlier this month, it’s hard to see how the private equity buyers make an adequate return at the kind of price point that would appeal to Kansas City Southern management and shareholders. The stock price reached a new high on the takeover speculation, but it was on the rise before that as investors bought in to the company’s pivot to precision-scheduled railroading, an efficiency strategy that aims to reduce the capital, cars and labor needed to run a train. The company’s foothold in Mexico is unique and makes for a good bet on the reshoring theme, but it’s not without risks amid Mexico President Andres Manuel Lopez Obrador’s threat to reverse reforms to the country’s energy industry.

BONUS READING

Amazon Drivers Are Hanging Smartphones in Trees to Get More Work

Airlines Fly Gadgets and Sea Trout to Fill Passenger Void

A Rust Belt Town’s Loyalties Divide as Pennsylvania Turns Purple

Taxing Robots Won’t Help Workers or Create Jobs: Noah Smith

Amazon’s Drone Delivery Fleet Hits Milestone With FAA Clearance

Aviation Job Losses Could Approach a Half-Million by Year’s End

The Great New York City Exodus Isn’t Really That Big: Justin Fox

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Brooke Sutherland at bsutherland7@bloomberg.net

To contact the editor responsible for this story:

Beth Williams at bewilliams@bloomberg.net