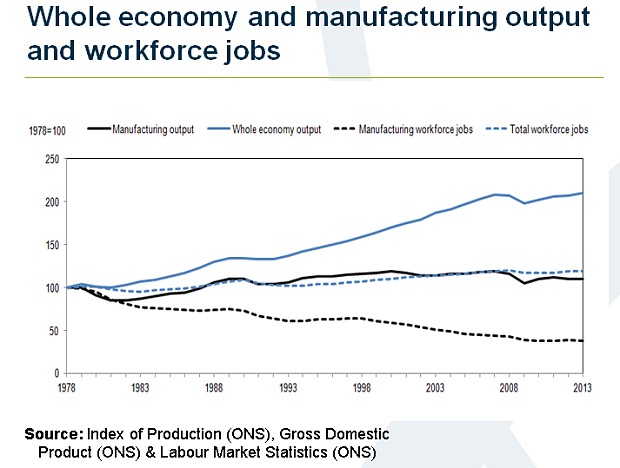

There is, of course, nothing new about de-industrialisation. Since 1978, the number of jobs in manufacturing has shrunk from 25pc of the UK workforce to around 8pc. Fewer than 3m people today work in UK manufacturing, against more than three times that number 40 years ago. Manufacturing output as a share of GDP has fallen by a similar order of magnitude. Surprisingly little of this displacement has ended up in financial services. The vast bulk of the outflow, at least in terms of jobs, has been into wholesale, retail, hospitality, government services, real estate, communications and transport.

All very depressing. Yet we should also be careful not to overstate the nature of the problem. As Sir Richard Lapthorne, who chaired a government sponsored review of the future of manufacturing a few years back, points out, manufacturing is not what it was. Big changes are under way that put a whole new light on what we think of as the manufacturing sector. The bald statistics don’t yet properly reflect these changes.

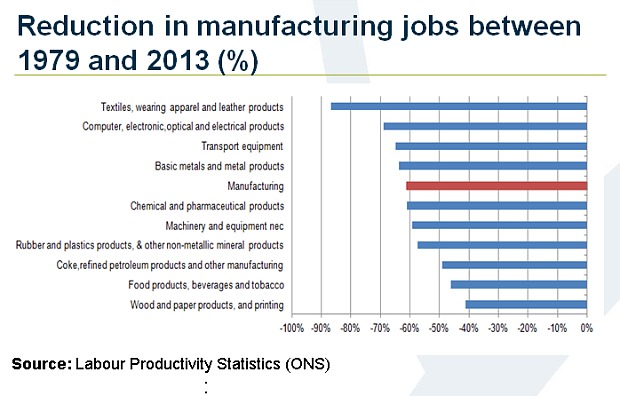

For a start, manufacturing is becoming very much more capital intensive. Developments in robotics and other forms of mechanisation are levelling the playing field and destroying the comparative advantage enjoyed by China and other low labour cost producers. This is already leading to some “onshoring” of production, particularly in textiles, an industry laid to waste by emerging market competition. However, these developments also mean that even if manufacturing were to make a big comeback in the UK, it would be unlikely in itself to create many jobs. Mass, production line employment is increasingly a thing of the past.

But it is in so-called “factoryless” production that the more significant changes are taking place. This is partly about outsourcing. Dyson, for instance, produces nothing in the UK at all, but all its research and development, together with its engineering know-how, is based here. The high-end value creation resides in Britain, not Malaysia, where the vacuum cleaners are produced. The same is true of Apple, which is essentially just a product development, quality control and marketing company. It makes hardly anything itself. ARM is a British version of the same thing; it designs and sells computer chips for smartphones, but it doesn’t make them.

It is in any case quite wrong to think of the modern manufacturer as solely about the process of turning base metal and biomass into saleable products. Most manufacturers today contain some service element. According to Sir Richard’s report, some 39pc of UK manufacturers with more than 100 employees now derive value from service activities. For Rolls-Royce, around half of revenues come from servicing and leasing its jet engines, rather than selling them.

The so-called “shared”, or “circular”, economy promises further expansion of this service-based element. Having seen the future, both Ford and BMW have dipped their toes into the market for shared cars, even though this seems to be at odds with the priorities of the traditional “take, make, consume and dispose” manufacturing model.

Value is progressively shifting from traditional manufacturing to idea-intensive businesses and industries. These tend by their nature to be more service based.

None of this is to argue that manufacturing no longer matters. Germany this week announced another record trade surplus. Britain’s economic recovery has meanwhile become worryingly dependent on an equally sizeable current account deficit, which can only persist without mishap as long as foreign capital is prepared to fund it. More can and should be done to encourage Britain’s tradable goods sectors. A good starting point would be to make all capital expenditure an immediate offset against revenue for tax purposes, thereby better aligning the incentives for capital investment with those of spending on labour.

Introduction of a national living wage may help a little on this front. But to succeed like Germany in manufacturing, companies need to be thinking in terms of a continuous process of multiple product launches, requiring heavy upfront investment in development and retooling. Despite nascent signs of recovery in capital spending, British industry is still underinvesting on a destructive scale.

Still, I began by referring to “silver linings”. As it happens, the terms of trade are once again moving quite dramatically in Britain’s favour, with the cost of energy, raw materials, food and many finished goods getting relatively cheaper, while the price of services is again rising fast. Pricing power significantly favours the UK’s areas of comparative advantage over those activities in which it is relatively weak. Certainly mass manufacturing no longer looks a good place to be.

Many of Britain’s service industries – particularly high-end business, financial and IT services – are in high demand the world over and can be easily exported. Britain might not produce very much any longer, but it is relatively well placed, possibly uniquely so, to benefit from these post-industrial trends, even as they apply to manufacturing.

Source Article from http://www.telegraph.co.uk/finance/economics/11851629/Unbalanced-but-lucky-Britain-hits-an-economic-sweet-spot.html